New Business Direction LLC

New Business Direction LLC Do you know if your marketing efforts are paying off? More importantly, do you know which marketing campaigns and channels are profitable and which are losing money?

Do you know if your marketing efforts are paying off? More importantly, do you know which marketing campaigns and channels are profitable and which are losing money?

Marketing is one of the toughest areas to calculate return on investment, and one of the reasons is because  customers may have had contact with your company in multiple ways before they make a purchase. Other reasons such as a lack of systems are more easily solved and can give you valuable information that you can make smart decisions with.

customers may have had contact with your company in multiple ways before they make a purchase. Other reasons such as a lack of systems are more easily solved and can give you valuable information that you can make smart decisions with.

One main goal of marketing is to acquire leads that will hopefully turn into buying customers and even repeat customers. To start measuring your marketing efforts, we need to find out where those leads are coming from and measure which ones became your customers. That means we need to develop a system that tracks a customer from lead source to sale.

The hard part is that some of this needs to be done outside the accounting system. The good news is that there are many tools and analytics available to help in this process.

One of the first things to do if you don’t already have it set up is to record the lead when they enter your sales process. Enter basic information about them in your CRM (customer relationship management system), and be sure to ask them how they found out about you. This will help you track the lead back to the campaign or channel that they came in on. Once they’ve made a purchase, you can connect the lead to the customer record and track revenue by marketing source.

If your leads come in digitally, there are many automated tags you can set up to track where they originated, whether it was from the web site, a particular web page, a social media account or a link from an email you sent.

An important statistic for businesses is cost per lead, how much it costs to generate one lead for your business. The cost will vary by channel or marketing source. For example, someone coming from your website will cost less than someone coming from social media in most cases.

Once you know how many leads to generate to make a sale, you can start calculating what your marketing budget should look like. More importantly, you’ll be able to forecast your revenue more accurately, too.

While numbers are probably the last thing you think about when you’re doing your marketing, they can be very effective for your bottom line. There are many metrics beyond cost per lead that would be valuable to measure as well. Here are just a few of them:

- Number of leads (in total or per channel)

- Number of press mentions

- Number of direct mail pieces sent out

- Number of email subscribers

- Number of social media connections per platform

- Number of posts sent, number of shares, number of comments

- Total web visitors, new and returning

- Google rankings for keywords

- Number of customer reviews per site, ratio of positive to negative reviews

And as always, if you want help developing these processes and metrics, please reach out.

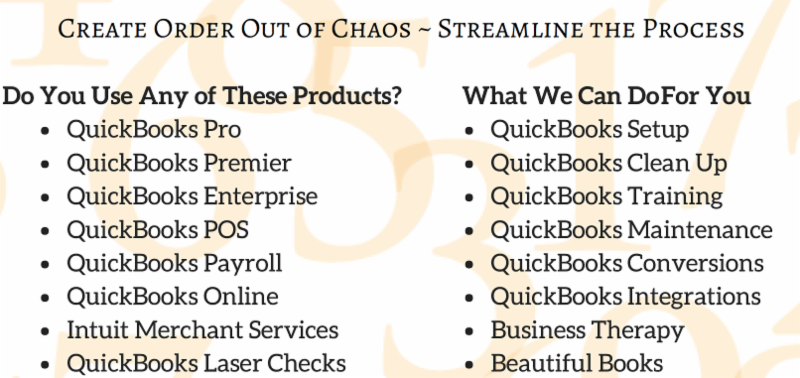

QuickBooks® will be sun-setting the 2016 Pro, Premier and Enterprise versions of their software as of May 31, 2019.

What this means for you? No more software updates from Intuit, no more hosting and no more support on the 2016 and earlier versions.

In addition, certain features will no longer be available in your QuickBooks® 2016 after May 31st – payroll processing, bank or credit card download links or the ability to email reports from within the software.

Now is a good time to evaluate your software needs, and we’re here to help.

As the source for all of your Intuit needs, let us help you! As always, we’re here to help make sense of QuickBooks®.

![]()

Many people in their retirement years have regrets about not saving more during their earning years, but you don’t have to be one of them. All you need to do is be realistic and proactive about saving. It’s all about paying your future self.

Circumstances can arise that can erode savings you hoped would be there for retirement. Some of those events include not being able to work due to poor health or a bad job market, unanticipated hospital bills, a divorce, overestimating Social Security benefits, bad investments, procrastination, and simply not realizing how much you need to live on.

The good news is you can prevent future regrets by making a strong savings plan now. As a small business owner, you may not have a retirement plan, so it’s essential that you create one for yourself. You earn an income today. Put some of that income toward paying your future self, and pay that “bill” first, every month or with each paycheck.

To be proactive and build as much savings as possible, take these steps:

- Increase your financial skills by learning how to fund your retirement.

- Take care to manage your investment risk and be realistic about investment returns.

- In good markets, purchase rather than rent or lease so you are building an asset.

- Put as much aside as you can, and live beneath your means.

- If you have periods when work is slow, live frugally until your income is back to normal.

- Optimize your business profits and apply some of them to your savings plan.

- Minimize taxes where possible so you can keep more of what you make.

- Make everything work twice as hard for you:

- Get credit cards with loyalty programs.

- Sign up for frequent customer programs to earn points.

- Make sure your bank is giving you the best deal on interest.

- Sell unused belongings on eBay and put the money into savings.

- Cancel subscriptions and memberships and move the saved money into savings.

- Periodically reach out to vendors to get a better deal on the expenses you incur. This could be for phone plans, utilities, and any other routine expense. Put the difference saved into savings.

- Select cars and trucks with good gas mileage and also high resale value. Consider that using Lyft or Uber may be cheaper than maintaining a car, depending on how much you drive. Put the difference in savings.

There are hundreds more ways to save more. These will get you started in the right direction for 2019.

The start of a new year also means that it’s the perfect time to revisit old business strategies from last year so that you can maximize your revenue for 2019. If your financial numbers were fantastic last year, that’s great! Keep the strategies that worked for you and cut the ones that didn’t.

If your financial numbers weren’t amazing last year, or maybe you’re just interested to see how you can increase your revenue, we have you covered. Here are 10 ways that you can boost your revenue this year:

- Revisit your current prices and make adjustments as necessary.

Many people will tell you that increasing your prices will increase your profits, but that’s not necessarily true. Increasing your prices by a small amount might increase your profits without turning away existing customers, but make sure you research your value and your competitors’ prices and adjust based on what makes sense in your market.

- Bundle your services or products together.

Make your products or services more attractive by bundling them together and pricing them at a better deal than purchasing the services or products separately. Customers who only want one particular product or service should still be able to purchase the product or service à la carte, but offering different packages of increasing value makes it much easier to upsell to customers and increase your business revenue.

- Offer free gift with purchase.

Tacking on a complimentary or free service to your products or services could be the small push needed to close sales. Even better, you could add a complimentary or free service to your highest-quality bundle. As an example, the cosmetics industry has been doing this for decades.

Tacking on a complimentary or free service to your products or services could be the small push needed to close sales. Even better, you could add a complimentary or free service to your highest-quality bundle. As an example, the cosmetics industry has been doing this for decades.

- Start a new product or service line.

If you’re limited to just a few products or services, it’s time to expand. If you mow lawns, offer a leaf collection or snow removal service. If you sell shoes, add socks. If you manage a restaurant, consider offering adult beverages. Expanding the scope of what you’re selling will provide you with additional revenue.

- Expand your geographic reach.

If you’re still only offering services and products locally, consider expanding your reach, especially because the internet is so readily available nowadays. Think about which services you can offer virtually; some may require you to invest in cloud-based delivery systems. If you only sell products at a physical location, ecommerce is a huge industry and you could definitely increase revenue by having a storefront online.

- Learn to say “no” to bad clients.

This may seem counterintuitive, but learning to turn away bad clients is really important. When customers are unresponsive, ungrateful, unreasonable and just take up too many of your resources, you have to realize that they are unprofitable. By turning them away, you can devote more of your attention to building relationships with your best customers and creating new, profitable opportunities.

- Make your online presence known.

Everyone uses search engines and social media to find the right business to serve their needs, so make sure you can be found online. Create a website for your business and make sure you have business pages on social media platforms like Facebook, LinkedIn and Twitter. You’ll have to develop some marketing strategies and optimize your site to rank high, but, when done right, these channels can drastically impact the amount of revenue you receive.

- Manage your online reputation.

When you have many good reviews, your credibility goes up and your business is more appealing to potential customers. If your clients leave you an amazing testimonial, it’s a good idea to ask them to post it online as well—especially on Trip Advisor, Yelp, your Facebook Business Page, and Google Reviews. On the other hand, negative reviews will look bad to potential customers and can negatively impact your revenue, so make sure you respond appropriately to the review and show potential consumers that you care about getting things right.

- Encourage customers to sign up for a continuity program.

Do you have loyal customers? Reward them by offering a membership or continuity program with VIP benefits. Retail, restaurants, and service businesses can set up privileges like faster service, discounted prices, and frequent purchase rewards that many consumers will pay a small monthly fee for.

- Encourage customer referrals by building and nurturing relationships.

Connect with customers and build strong relationships through effective communication, providing exceptional service, getting feedback, addressing concerns, and showing appreciation. Doing so can increase repeat customers, customer referrals and your business revenue.

If you’re looking to boost your business revenue this year, definitely give these strategies a try. If you would like specific suggestions for your business, please reach out.

One of the biggest challenges for small businesses is managing cash flow. There never seems to be enough cash to meet all of the obligations, so it makes sense to speed up cash inflows when you can. Here are five tips you can use to get your cash faster or slow down the outflow.

One of the biggest challenges for small businesses is managing cash flow. There never seems to be enough cash to meet all of the obligations, so it makes sense to speed up cash inflows when you can. Here are five tips you can use to get your cash faster or slow down the outflow.

- Stay on top of cash account balances.

If you’re collecting money in more than one bank account, be sure to move your money on a regular basis when your balances get high. One example is your PayPal account. If money is coming in faster than you’re spending it, transfer the money to your main operating account so the money is not just sitting there.

your money on a regular basis when your balances get high. One example is your PayPal account. If money is coming in faster than you’re spending it, transfer the money to your main operating account so the money is not just sitting there.

- Invoice faster or more frequently.

The best way to smooth cash flow is to make sure outflows are in sync with inflows. If you make payroll weekly but only invoice monthly, your cash flow is likely to dip more often than it rises. When possible, invoice more frequently or stagger your invoice due dates to smooth your cash balances. Or consider changing your payroll schedule to bi-weekly.

Take a look at how long it takes you to invoice for your work after it’s been completed. If it’s longer than a few days, consider changing your invoicing process by shortening the time it takes to send out invoices. Email invoices to your customers with a payment link. That way, you’ll get paid sooner.

- Collect faster.

Got clients who drag their heels when it comes to paying you? Try to get a credit card on file or an ACH authorization so you’re in control of their payment. Unless you have a compelling business reason, there is no need to extend 30 days to pay you. Change your payment terms to Net 7, 10 or 15 days.

Put a process in place the day the invoice becomes late. Perhaps the client has a question or misplaced your bill. Be aggressive about following up when the bill is past due. Turn it over to collections quickly; the older the bill is, the less likely it is to get paid.

- Pay off debt.

As your cash flow gets healthier, make a plan to pay off any business loans or credit cards that you have. The sooner you can do this, the less interest expense you’ll incur and the more profit you’ll have.

Interest expense can really add up. If you have loans at higher interest rates, you might try to get them refinanced at a lower rate, so you won’t have to pay as much interest expense.

- Reduce spending.

You don’t always have to give up things to reduce spending. Look at your expenses from last year and ask yourself:

- What did you spend that was a really great investment for your business?

- What did you spend that was a colossal mistake or waste of money?

- What do you take for granted that you can cut? What services are not being used?

- Where could you re-negotiate contracts to save a little?

- Where could you tighten up if you need to?

Managing cash flow is always a challenge, and these tips will help give you a little cushion to make it easier. If you would like us to help with specific suggestions for your business, please reach out.

Sign up for our FREE newsletter

Tips & Tricks in QuickBooks®