New Business Direction LLC

New Business Direction LLC

If you have accumulated more money in your business checking account than you need for daily operating expenses, congratulations! That is an excellent “problem” to have! It could be time to consider putting that money to work for you. A business savings account can help small business owners plan for the future and ensure financial security. It can provide a protected place to set aside funds, allowing you to save for a rainy day, prepare for less prosperous seasons, invest in new equipment, or take advantage of opportunities that may arise.

A business savings account can also provide you peace of mind, knowing that money is available when needed. In addition, access to higher interest rates and the ability to transfer funds quickly is a great way to help ensure greater financial security for the business.

Every banking institution is different when it comes to the features and benefits of its business savings offerings. We’ve assembled a list of common questions you may want to consider asking your banker before opening a savings account:

- Is your checking account interest-bearing, and if so, how does the interest rate compare to that of a business savings account?

- Is there an initial minimum deposit to open the savings account?

- What are the monthly fees for each type of account?

- What minimum balances are required in both checking and savings accounts so that fees are waived? And, would it be worth it to keep minimum balances?

- Are there withdrawal limits?

- What are the other benefits of having a business savings account with your institution?

- Is my money FDIC-insured, and if so, what is the cap?

Often, a bank will tie the checking and savings accounts together, and there will be a combined minimum balance that is lower than if either account was separate. For that reason, having your checking and savings accounts in the same bank might be more effective. Other common benefits include waiving overdraft fees, wire transfer fees, and NSF charges.

There are other types of interest-bearing accounts besides savings accounts, including money market accounts and certificates of deposits (CDs).

A money market account is a type of savings account that allows you to earn a higher rate of interest than a traditional savings account while also providing you with access to your funds. It may have check-writing privileges, but the withdrawals may be limited. Certificates of deposits, or CDs, typically pay higher interest rates than traditional savings accounts. Still, they tie up your money for a specified period, and steep early-withdrawal penalties exist.

Many institutions besides your primary bank are focused on savings accounts and will pay much higher interest rates. For example, online banks and credit unions typically pay a higher interest rate than a brick-and-mortar bank; however, the money may not be FDIC-insured, so be sure to read the fine print.

An additional benefit of keeping money in a separate savings account is that you can save for many things:

- A cushion for emergencies.

- Lump sum tax payments.

- Future capital expenditures.

Once you’ve set up your new savings account, consider scheduling recurring transfers to it so that you build up your savings balance.

A business savings account is a great way to ensure your business is prepared for unexpected costs, expenses, or growth opportunities. With a business savings account, you can put your unused funds to work, earning you higher interest than a checking account could. By incorporating a savings account that works for your business’s needs, you can feel more secure about the financial future of your business.

As business owners, we’d like to think that we make rational, logical decisions regarding our business finances. However, scientists have discovered hardwired biases in our minds and thought processes, one of which is the sunk cost bias, also known as sunk cost fallacy.

A sunk cost is simply money, time, or resources you have already spent and can’t recuperate. Another word for them is retrospective costs. The bias comes into the picture when we consider those costs in future decisions.

The sunk cost fallacy, first hypothesized by Richard Thaler in 1980, is a cognitive bias where people overestimate the importance of sunk costs in their decision-making. He wrote, “Paying for the right to use a good or service will increase the rate at which the good will be utilized.”

In a 1985 paper by Hal Richard Arkes and Catherine Blumer titled “The Psychology of Sunk Cost,” the authors found evidence that this tendency is “predicated on the desire not to appear wasteful.” Furthermore, “those who had incurred a sunk cost inflated their estimate of how likely a project was to succeed compared to the estimates of the same project by those who had not incurred a sunk cost.”

Essentially, instead of making a decision that’s right for themselves and their future based on current circumstances, people will make a decision heavily informed by the action already taken, even when it isn’t relevant to current circumstances. It doesn’t sound very productive, does it?

Let’s discuss two examples of the bias in action. First, let’s say you have spent a lot on car repairs. You continue to repair the car, digging a deeper and deeper hole. Making a $3,000 downpayment toward purchasing another vehicle is likely a better decision than sinking the same amount of money into another round of repairs. However, you are still emotionally (and irrationally) attached to all the money you spent on the clunker.

Now say you have an employee that is a borderline performer. You keep investing in them, thinking you can “fix” them. However, they don’t improve. Regardless of whether the employee is insubordinate or simply not the right fit for the role, letting them go was likely the right move to make some time ago.

So, now that you know about the sunk cost bias, how can you avoid falling into it in your business? Here are some ideas:

- Increase your mindfulness when making decisions that involve costs already incurred. Ask yourself, “what decision would I be making if I hadn’t already invested the time/money/resources into this project?”

- Since the bias can often come as the result of not wanting to experience negative emotions like feelings of failure, irresponsibility, or loss, try to remove your emotions from the equation altogether. Instead, examine the business project at hand from a facts-only perspective. Ask yourself, “What does the data show me?” Then do the math.

- Track key performance indicators (KPIs) regularly to see whether you’re on or off track and assess whether it’s worth continuing the project sooner.

- Like setting a budget for holiday shopping, establish goals and milestones for future projects, and have a “walk away” plan if things spiral out of control.

- Stay future-focused.

Ultimately, it will be up to you to ensure that sunk cost bias doesn’t affect your decision-making in the future. Hopefully, this information and the five tips we provided will help you orient yourself to make business decisions that benefit current and future you, rather than past you.

If you’d like to learn more about cognitive bias, including the sunk cost bias, check out the works of two additional scientists, Daniel Kahnerman and Amos Tversky (the former of whom won the Nobel prize for his work!).

Are you looking for new ideas to market your business? Knowledge panels might be an excellent tactic to consider. If you haven’t heard of them, don’t worry; many people haven’t, but they are a Google invention widely used in search results daily.

Knowledge panels are the information panels that appear on the bottom right corner of your search results when you look up specific people or brands. They differ from the business profiles you see when you query a company, which Google Business Profile provides.

Knowledge panels display information that Google has collected in its Knowledge Graph, which is one of Google’s information databases. For example, search for a favorite author or your current Congressperson, and you can see an example of a knowledge panel. Famous historical figures and extremely popular entertainers may have a more robust page displaying all of the information about them, but there will typically also be a column of text to the right (you may have to scroll a bit to see it), which is the knowledge panel.

So, how can you use knowledge panels in your business? A knowledge panel representing your leadership or brand brings instant credibility and visibility to your organization. It boosts reputation and helps to build trust with all stakeholders.

Who typically has a knowledge panel? If you happen to be an author of a book with a formal ISBN (International Standard Book Number), you would automatically get one. If you are a leader of certain organizations, like Bob Iger of the Walt Disney Company, you will also get one. If your brand is well-known, it will have a knowledge panel.

You can’t create a knowledge panel, but you can claim it once it appears. Google determines who receives a knowledge panel. But you can “lobby” for one, and there are marketers you can hire to help you execute the steps it takes to get one. The main thing is to be active and visible online.

If you already have a knowledge panel, there are procedures documented on Google Help that you can follow to claim it. You can also make edit suggestions and submit them to Google. You can’t directly edit your knowledge panel, however; Google has final control over what is displayed.

After reading this article, we hope you now have a good jumping-off point to understanding and obtaining a Knowledge Panel. With so many marketing tactics available online to help promote your business, it’s essential to stay in the know about them!

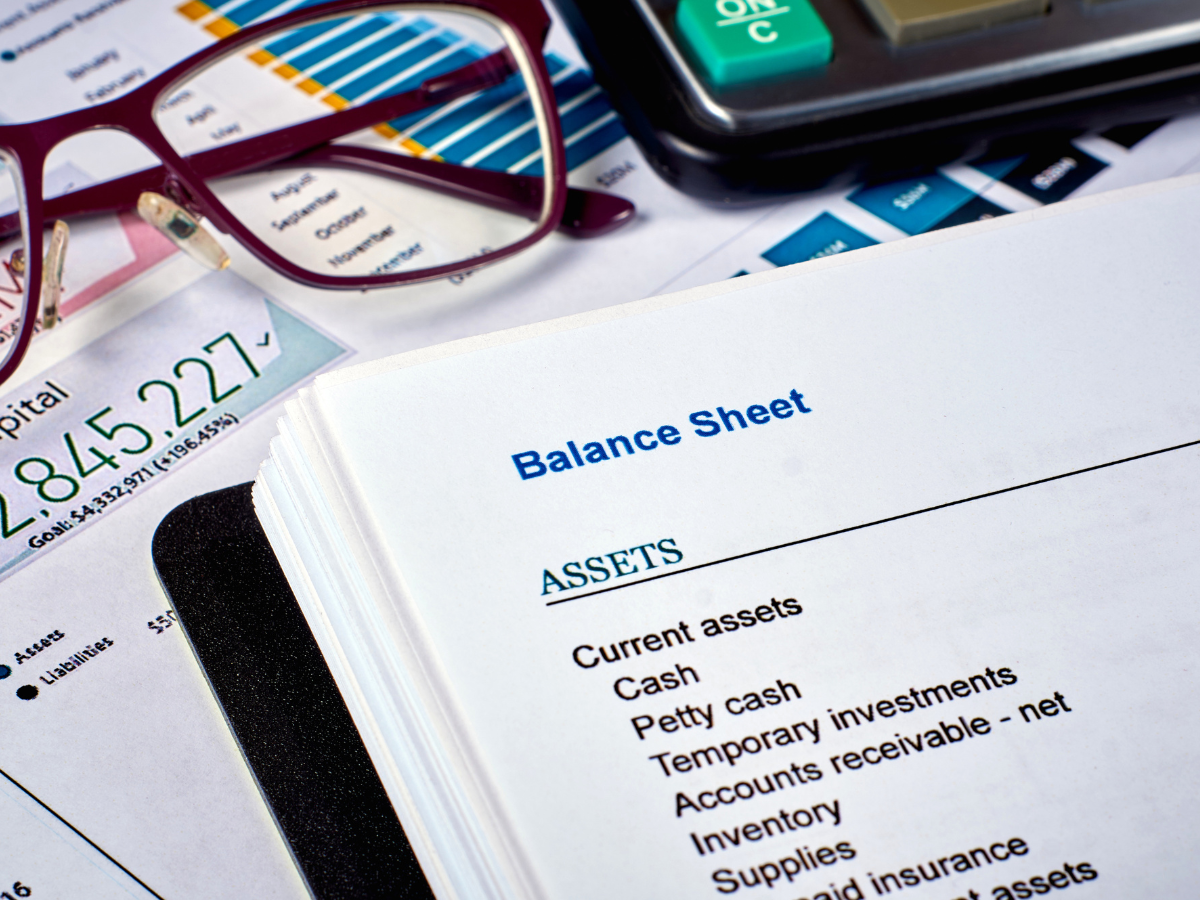

A balance sheet is a financial statement showing a company’s assets, liabilities, and equity at a specific point in time. It’s one of the foundational financial reports for your business. But did you know the equity section of the balance sheet looks different depending on a business’s legal structure? The most common entity types are corporations, partnerships, and sole proprietors. Recently, we discussed what equity looks like on a corporate balance sheet. This time, we’ll review what the equity section of the balance sheet looks like for sole proprietors.

A balance sheet is a financial statement showing a company’s assets, liabilities, and equity at a specific point in time. It’s one of the foundational financial reports for your business. But did you know the equity section of the balance sheet looks different depending on a business’s legal structure? The most common entity types are corporations, partnerships, and sole proprietors. Recently, we discussed what equity looks like on a corporate balance sheet. This time, we’ll review what the equity section of the balance sheet looks like for sole proprietors.

The Equity Section

The equation Assets = Liabilities + Equity is true for all entities. For a sole proprietor, equity is called Owner’s Equity. There are typically two accounts listed: the Owner’s Capital Account and Owner’s Draw Account. We define both below.

Owner’s Capital Account. This balance represents how much money the owner has put into the business. Also included are cumulative business income or loss amounts from prior years.

Owner’s Draw Account. This balance represents how much money the owner has taken out of the business. Since a sole proprietor does not get a paycheck, taking money out of the business via a draw is how they receive their money.

A third account will show up if you run a balance sheet report in your accounting system on any date during the year: Current Year Earnings. This balance is the same as the net income on the year-to-date income statement. It represents the profit of the business.

On a formal balance sheet for external purposes, only one account will show: the Owner’s Capital Account. This is because the draw and the current year’s earnings will roll into that account.

Salary vs. Draw

It’s important to distinguish between the concepts of a salary and a draw. In corporations, owners receive salaries in the form of paychecks, where payroll taxes are deducted, and W-2s are issued at year-end. In the corporation’s income statement, the salary and taxes are deducted as expenses.

For a sole proprietor, this is not at all how it works. A sole proprietor has no salary. Therefore, there is no payroll expense or payroll taxes on the income statement for the owner. The owner could have employees, and those payroll expenses would be shown on the income statement, but there is nothing for the owner.

Instead, the owner takes draws, which are not an expense; they’re simply a reduction in equity. They do not affect profits or change taxes owed. An owner can take a great deal of money out of the business, and there is no impact on profits. There is undoubtedly an impact on cash flow, however!

A sole proprietor does pay payroll taxes in the form of self-employment taxes. They simply do it on their IRS Form 1040 as opposed to payroll tax forms that a corporation would use.

The equity section can be the most challenging to understand on the balance sheet. Hopefully, the explanation above will provide more clarity so you can better understand how to read your business’s financial statements.

Running a business can be incredibly rewarding, but it can also be incredibly exhausting. As a business owner or manager, it’s essential to take the time to slow down, recognize when you’re feeling overwhelmed, and take proactive steps to reduce fatigue and burnout. In this blog post, we’ll explore the importance of sustainable business practices and how slowing down can help protect your physical and mental health while supporting organizational success.

1. Eliminate wasted time.

Take a thoughtful look at your to-do list. Are there any tasks that take significant time and resources to complete that don’t offer you the return on investment to make them worthwhile? What would happen if you eliminated them from your to-do list entirely? Would you still meet your desired destination? If yes, it may be time to axe that task. Consider this quote from The Four Disciplines of Execution: “The only reason you fight a battle is to win the war.” Is this task going to help you win it? Or does it just feel productive?

2. Get off electronics and social media.

Vision Direct polled 2,000 adults in the U.S. and found that the average person spent over 6,259 hours per year staring at screens. If that statistic is making you sweat, or if you feel like you don’t have any time to live the life you want to, your work-life balance could be lurking behind the electric glow of your devices. Instead of setting an ambiguous goal to use your cell phone less, try tactics like:

- plugging your phone in overnight in a different room to prevent you from starting your day by doom scrolling

- Setting an alarm at night to set the phone down and enjoy some ‘analog’ activities

- Utilizing your phone’s screen time features to remind you when you’ve spent a certain amount of time on any one app.

- Turning your phone off and putting it away for–gasp–an entire weekend day.

3. Get enough sleep.

Sleep deprivation can negatively impact your executive functioning abilities. If you are sleep-deprived, everything takes longer. Mistakes happen more frequently. Emotions become hard to regulate. Slowing down and getting enough sleep each night can make you more productive, reducing work hours. Plus, you feel more refreshed.

If getting to bed an hour earlier isn’t feasible for you, could you find time to rest your eyes for 15 minutes a few days a week? According to the Sleep Foundation, “A nap can improve cognitive functions such as memory, logical reasoning, and the ability to complete complex tasks.”

4. Zoom out to gain a new perspective.

It’s called the hamster wheel for a reason: you’re moving so fast you can’t see that you aren’t actually going anywhere. Slowing down your usual routine can help you gain perspective. Now that you’ve cut out superfluous tasks, cut down on screen time, and are getting more rest, use that extra bandwidth to reconnect with your mission, vision, and purpose. You might have been fighting fires in the trenches for so long that you’ve forgotten why you’re in business. Make sure your employees understand their grander goals as well.

5. Avoid multitasking.

By this point, we’ve all heard the data that multitasking doesn’t actually save time. But are you executing the discipline to work on tasks one at a time, or are you task-switching in rapid succession? Almost everyone thinks they are good at multitasking, but a study by Jason M. Watson and David L. Strayer concluded that only 2.5% of people can multitask effectively.

Becoming self-aware of your habits related to multitasking is the first step. Next, consider batching your work by client or task type. Note when you’re feeling more energized throughout the day and when your attention seems to lag. Then plan your work accordingly. This process is called capacity planning or time batching, and we have an entire article dedicated to it here. The key is to continue experimenting within the framework and see what works best for you.

6. Get better at managing distractions.

If you get interrupted every five minutes, you will feel drained of energy at the end of your work day. Get smart about managing interruptions so you can be more productive. You can try strategies like:

- Setting your phone to “do not disturb.”

- Carving out time on your calendar as “unavailable” so teammates don’t have total access to your time.

- Placing your phone somewhere you can’t mindlessly reach for it.

- Turning email and chat notifications off.

- Working during an off time.

- If you’re in a physical office space, close your door.

7. Stop worrying about billable hours (for service businesses) – at least for a while.

If you’re feeling fixated on billable hours as of late, it may be time to take a step back, even if it feels counterintuitive. Otherwise, this preoccupation could affect the quality of service you’re able to offer your customers, which could lead to a decrease in customer satisfaction and hurt your reputation.

In addition, that constant attention on billable hours might even be causing you unnecessary stress. It’s not sustainable for every season of your business to be one of exponential growth. Sometimes, holding fast for a quarter can give you time to reevaluate your priorities in your business and personal life. This, in turn, can allow you to step forward confidently when the time is right.

8. Do nothing.

It’s actually okay to do nothing sometimes when you’re the business owner. Your mind needs space to develop new ideas, think about creative solutions to complex issues, and even daydream. Does the act of doing nothing leave you feeling incredibly uncomfortable? Then it’s probably exactly what you need.

By implementing these new strategies to free up time, you’ll find you’re better able to take back control of your day and slow down. Slowing down in your business is essential for your mental and physical well-being. Taking the time to rest, recharge, and evaluate your goals will allow you to refocus and realign with your purpose. When you are in a state of balance, it becomes easier to make decisions that benefit your business and your life.

And just as importantly, slowing down allows you to enjoy the fruits of your labor, appreciate the moments of success, and celebrate the milestones you have achieved.

How do you arrive at a price for the products and services you sell? While it depends on what industry your business is in, a handful of foundational pricing methods will be useful regardless of your business model. We outline five: time and materials pricing, cost-plus pricing, market pricing, target pricing, and value pricing. Let’s dive into each one.

Time and Materials Pricing

Time and Materials (or T&M) pricing is a method used by many service-based organizations. As you might have guessed, T&M pricing is based on the time spent performing the service. A few great examples of Time and Materials pricing include the hourly rate an attorney charges, the rate a massage therapist charges for a 50- or 80-minute service, or the minimum fee a plumber charges, plus a different rate for subsequent hours. It’s also a method typically used in construction and product development.

In some cases, time-based pricing may be loosely tied to the salary level of the person performing the service. Still, there must be a substantial markup to cover payroll taxes, health insurance, overhead, training, and any materials or tools that are included. While costs like hourly rates, materials, equipment use, and independent contractors are typically agreed upon by the provider and customer ahead of time, the customer won’t usually receive an estimate in advance.

Cost-Plus Pricing

Cost-Plus pricing (also referred to as Markup pricing) is typically used in the retail industry. Retailers select inventory from a manufacturer or wholesaler and then make those products available to the public for purchase. This method is based on unit cost plus a markup. A typical example is keystone pricing, when an item is marked up to twice the purchase price plus one dollar.

Other industries that use cost-plus include groceries and auto dealers, but the pricing approach would also be relevant to businesses like a bakery, which purchases inventory in the form of ingredients and transforms them into a new product, like a pie.

Market Pricing

Market pricing is the act of establishing the price for your goods or services based on the rates your competitors are currently offering. It is dependent on fluctuating market conditions and allows the seller to stay competitive with other providers. Commodities are the best example of Market pricing: Crops, oil and gas, and metals are all priced by the market.

Target Pricing

Target pricing is the process of beginning with a price that you feel customers will be willing to pay, and then designing a service or product around it. It’s commonly used in the SaaS, or Software as a Service, industry.

For example, let’s say you develop a concept for a subscription-based application that you believe consumers will pay a competitive rate of $29/month for–note that this price will be based on market research, not a ‘gut feeling.’ You would then build your application (and the resources required to support it) around a budget driven by the target price. If an organization can’t create the application build within the budget, it scraps the project.

When an organization takes the Target pricing approach, it can be more confident of a reasonable profit because the price is already consistent with market demand.

Value Pricing

Value pricing is based on the price a customer is willing to pay and what they value, rather than the direct cost of the product. For example, a customer with more to gain from employing your services is likely willing to pay more than a customer of smaller means with less to gain. This is because, while both customers may receive the same services, their perceived value of your services is different. Thus, they’re willing to pay different prices. For project-based work, Value pricing can be based on the customer’s expected return on investment (ROI) and is used in digital marketing and for some professional services.

Pricing in Action

In business, determining a product or service’s price is part math and part art. It may even be a combination of two or more methods listed above. There are many factors and considerations that will inevitably go into your pricing decisions. New Business Directions can help you determine if your prices are adequate for the profit margins you want, competitive with your industry’s standards, and more. We can also help with if-then scenarios. For example, if you raised your rates by $100 an hour, but demand went down five percent, what would your profit margins look like? Please reach out to us to schedule a paid consultation if you would like us to help you with your pricing process.

By now, you’ve probably seen the new buzzword “Quiet quitting” floating around. Coined in 2022 and popularized through TikTok, the term refers to an employee who remains working but reduces their performance to the bare minimum required to keep their role.

By now, you’ve probably seen the new buzzword “Quiet quitting” floating around. Coined in 2022 and popularized through TikTok, the term refers to an employee who remains working but reduces their performance to the bare minimum required to keep their role.

On the other hand, critics of the term say that “quiet quitting” is simply accomplishing the essential duties and refraining from going above and beyond the job description without adequate compensation, avoiding the glamorization of hustle culture.

Whether a result of a favorable job market for employees or a new shift in priorities to a more sustainable work-life harmony, if you suspect quiet quitting is taking place at your organization, it could be time to take action. Instead of coming down harshly with written warnings or other punitive measures, consider a supportive leadership approach, addressing the root causes of employee dissatisfaction.

Keep reading for a few suggestions to get you started.

On the macro level:

- Implement employee wellness programs designed to reduce stress and improve physical and mental well-being, such as an incentivized movement challenge or free access to a mental health app like Headspace.

- Add some perks, such as a sponsored weekly, in-house yoga class or a program led by an instructor certified in mindfulness-based stress reduction methods.

- Encourage employees to take vacation time to reduce burnout. If an employee doesn’t feel empowered to take time off, there could be underlying issues in your company procedures that need to be addressed.

- Add training programs so that employees can have a chance to develop new skills.

- Add an education reimbursement program where employees can return to school and earn a degree or certificate related to their job.

- Ensure that employees’ health plans include a substantial mental health component.

- Partner with a child-care and/or senior-care agency to reduce the stress of finding support for families who need it. Providing care support will especially help women re-enter the workforce, as they have been impacted most by the increased care demands brought on by the pandemic.

- Bring back the company holiday party, annual picnic, or movie night so employees can socialize with each other again. If you have a fully or partially remote team, a virtual party during work hours is also a great option, and there are companies that can help you facilitate one that’s fun for all.

On the micro level:

On the individual level, and especially for team members you suspect could be quiet quitting, it’s a good idea to conduct a formal process of setting goals.While this is generally accomplished during annual or seasonal employee performance reviews, it doesn’t have to be. It can be very effective to sit down with an employee and simply ask what they want to get out of this job and what they want their future to look like. Have a conversation with team members.

Goal-setting encourages well-being and can give an employee something to strive for. In addition, refreshing goals quarterly can help a team member re-engage with their role. It can also help a supervisor identify an employee who might be happy doing another job, creating the opportunity for a reassignment that is advantageous for both parties.

Increasing Employee Engagement

Anything that can help to refresh and rejuvenate your employees will help reduce a culture of contempt in your organization. While many of these approaches come with some associated costs, it’s essential to consider the alternative cost of an underperforming team or even the cost of a new hire. So start your approach with an initiative that will have the most significant impact on the well-being of your team—and unless you’re already doing most of the above, that probably isn’t a pizza party or free SWAG.

A new year is a perfect time for a fresh start for you and your organization for many reasons, whether it’s a familiar milestone you celebrate with friends or the beginning of your organization’s fiscal year. Below, we lay out five ways you can welcome 2023 and make it your most intentional year yet.

1. Decide on a theme for 2023

Setting a theme for the year can help you refocus your efforts to align with your goal or mission throughout the year. Meditate on your progress in 2022, how you’d most like to spend your time in the new year, and any achievements you’d like to accomplish in the next 365 days. We’ve outlined a few suggestions to help get your creative juices flowing:

- Growth and improvements to your organization. Many business leaders want to see growth and improvement in their organizations, but it’s important to remember that there’s power in specificity. How do YOU want your organization to grow and improve? Quantify that statement; otherwise, you’ll be hard-pressed to stay focused on your theme.

- Downsizing, cleansing, or simplifying. Perhaps business has proliferated so much in the past year that you need to sit back, de-clutter, re-design, or even clean your office.

- Could it be time to launch that new service you’ve been dreaming of?

- Giving back. If everything is humming along nicely, now could be a great time to start giving back to your community through your time, services, or financial resources.

Once you’ve decided on your overall theme, create a plan of realistic tasks and timelines that align with your chosen theme.

2. Attend a retreat

If you need to regroup and rejuvenate from a stressful holiday season (or even stressful year) then a retreat can do just the trick. A retreat is a time to step out of your day-to-day responsibilities in order to set goals for your business and make a plan. Often, a retreat can afford us greater clarity in our direction and concrete steps to implement them.

A retreat can be made on your own or with a group of specific team members. Typically, the events of a retreat include a combination of planning and brainstorming sessions, education, team-building, and social activities.

If a retreat sounds like too much work, then a quick vacation (or even a staycation!) might be in order so that you can enter the new year with a relaxed mind.

3. Learn from 2022

If 2022 was bumpy for your business, now is a great time to perform a detailed review. Consider your wins and losses, review your finances, and determine opportunities to improve your service, product, internal procedures, or work experience. Doing so will help you learn what went wrong and explore why. From there, you can brainstorm ideas on how to learn from any mistakes and avoid making them in 2023. Consider making this process structured in a way that affords you the greatest clarity, such as an after-action review.

4. Select a word for 2023

If setting a theme is too complicated, how about selecting one straightforward word for 2023? Here are some ideas:

- Abundance (think big, go after large contracts and big projects, etc.)

- Creativity (think outside the box, innovate, incorporate design)

- Community (hone relationships, support marginalized groups, give back)

- Gratitude (celebrate small wins, reward your team)

- Service (support the community with your talents, volunteer at a local nonprofit, etc.)

- Fun (encourage play, add spontaneity into your workplace culture)

- Prosperity (create an equitable work environment, align your spending with your morals, fortify your organization for future generations’ benefit)

Once you think of the best word for your year ahead, make it impossible to forget by writing it on post-its, setting it as your phone background, or even incorporating it into your email signature to reinforce your priorities.

5. Make a profit plan (AKA forecast)

Making a profit plan for the new year will help you hone in on the profit amounts you want to achieve. Understanding how much volume you need to reach and what you can spend will avoid surprises at year-end. It’s good to reevaluate your standing on a monthly and quarterly basis, so you have time to adjust your deliverables, revenue, or expenses to meet your goals.

Whether you do one or all of the ideas listed above, we hope you have an exceptional 2023 and that it’s your best year ever, whatever that means to you.

The word “audit” can be thrown around often in workplace conversations. It could refer to a review of your organization’s digital media presence or the assessment of internal procedure effectiveness. However, when used by an accounting professional, the term “audit” has a precise meaning. Keep reading to learn more.

The word “audit” can be thrown around often in workplace conversations. It could refer to a review of your organization’s digital media presence or the assessment of internal procedure effectiveness. However, when used by an accounting professional, the term “audit” has a precise meaning. Keep reading to learn more.

Financial Audit

A financial audit is an official service designed to inspect an organization’s accounting records, technology, and processes. An audit can only be conducted by a licensed CPA who is independent of the organization, meaning that the CPA performing the audit must have no relationship with the organization, its owners, or its employees. This requirement exists to avoid any compromise to the audit or appearance of impropriety.

To conduct an audit, the CPA performs a set of tasks that review the company transactions, balances, and accounting processes, called an audit program. The audit program is custom-designed for the company based on the risks perceived by the audit team, the type of organization being audited, and other factors. Once the audit has been completed, the auditor will issue a formal report stating the findings of the audit. The report typically includes a letter, financial statements, and footnotes.

The auditor’s report can be utilized by the company’s management and third parties, such as lenders and stockholders.

While there are mandatory audit requirements for large public companies, government institutions, schools, and nonprofit organizations, these aren’t typically applicable for small businesses due to the expense. There are other assurance services that can be more helpful for small businesses. They include compilations, reviews, and agreed-upon procedures. Let’s learn more about them.

Other Assurance Services

An audit falls under assurance services in accounting, and it’s the most stringent of all. But there are other types of assurance services available, like:

Compilations. In this type of engagement, the CPA performs basic checks on your financial statements and puts them together with a cover letter. It basically tells a third party that you have a CPA, but it provides the least amount of assurance service.

Reviews. In a review, there are a few more checks, tests, and inquiries, that a CPA will perform before issuing financial statements. This service provides more assurance than a compilation but less than an audit.

Agreed-upon procedures. An engagement with agreed-upon procedures is a very specific engagement where one aspect of the business is reviewed in accordance with a specific goal.

When small businesses are asked for documents from an accountant by a bank or lender, they can often provide these lower-level assurance reports, and the reports will not only suffice but save money.

IRS Audit

The term “audit” can also be used informally to define an inspection more narrow in scope, such as an audit performed on an organization by the IRS or a state agency. There is no assurance provided in this type of audit. This audit aims to produce whatever records the organization is asked for to verify the numbers it sent to the agency. These types of audits can occur randomly or as a result of suspected fraud.

Audits performed by the IRS or a state agency can be stressful and unpleasant experiences. Having your accountant support you along the way can be reassuring.

All organizations, no matter their size, have bills to pay. The larger the company, the more formal the accounts payable process tends to be. That doesn’t mean small business owners can’t benefit from a formal accounts payable process. Establishing one can be a great way to set controls and avoid unnecessary and unapproved spending. Let’s look at the accounts payable workflow to see where we can put some controls in place to protect your organization’s hard-earned money.

All organizations, no matter their size, have bills to pay. The larger the company, the more formal the accounts payable process tends to be. That doesn’t mean small business owners can’t benefit from a formal accounts payable process. Establishing one can be a great way to set controls and avoid unnecessary and unapproved spending. Let’s look at the accounts payable workflow to see where we can put some controls in place to protect your organization’s hard-earned money.

Purchase Order

A good first step is to initiate a purchase ordering process. All spending over a certain amount, such as $500, should require pre-approval from a manager or officer of your company. This step can take the form of a purchase order.

A purchase order (PO) is simply a pledge on the part of your company to purchase an item or group of items from a particular vendor. It should include the vendor’s information, the item(s) and quantities, the price that the vendor has agreed to, and who initiated and approved the proposed purchase. It will look similar to a bill, but it’s not a bill and should be appropriately marked.

If the price is not standard or the items are custom, there may be an estimate from the vendor that documents the price on the purchase order. The vendor writes the estimate document, while your company originates the purchase order.

While the purchase order is important, it does not create any entry on your accounting records, as no transaction has taken place yet.

Bill

The bill is the documentation of the purchase with a payment request. It is created by the vendor from which you are obtaining goods or services. It should be recorded on your accounting books once you have received it from the vendor.

The bill should be matched with the purchase order, checking to see if each item, quantity, and price match the same on the purchase order. Any discrepancies require explanation.

The timing of the bill can vary. For example, you may receive it before or after you’ve received the goods or services it covers.

Packing Slip

If the goods ordered are physical and will be shipped to you, then a packing slip or shipping document will usually be included with your package. The shipping document will have quantities but may not have prices listed. The document should match the actual items received, and any shortages or overages should be noted.

A process to stock the items into your inventory should then occur. A transaction should be entered into your system to increase inventory for the goods you receive.

The (corrected) packing slip should be matched against the bill to ensure sure you have received everything included on the bill. Again, if there is a discrepancy, it should be noted.

It’s common for back-ordered items to come in a later shipment, especially when supply chains become disrupted due to the pandemic. If your organization deals with multiple shipments for a single order often, you’ll need to set up a process for tracking them.

Approvals

As you can see, there might be a couple new checks and balances for you to implement in your organization, and there should be a documented processes for each one: one for matching the documents, another for any discrepancies that arise, and a final one for approval as you move from purchase order to packing slip to bill.

Your workflow may vary from the one listed above, depending on the order the documents are received and when payment is required. You may even have a different workflow for different vendors.

Once the purchase order, shipping document, and bill have been matched and corrected, it’s time to get them approved for payment by the appropriate level of management that you desire. You’ll want to determine which of your employees can spend and approve certain amounts in advance of this step.

Payment

Once your bill is approved, review the payment terms and due date, then prepare the bill for payment. This can be accomplished through your accounting system or by using a company credit card, sending a bank transfer or wire, or writing, signing, and mailing a manual check.

Workflow

A strong accounts payable workflow will protect your company from unauthorized payments, missing items, and even hasty purchasing decisions. There are also many accounts payable systems to support the automation of this procedure so you can implement it with greater ease.

New Business Directions provides custom workflow development and training, so if you’re interested in refining your processes around accounts payable, visit newbusinessdirections.com/custom-workflow-development/ or reach out to us via our inquiry form, located on our contact page.