New Business Direction LLC

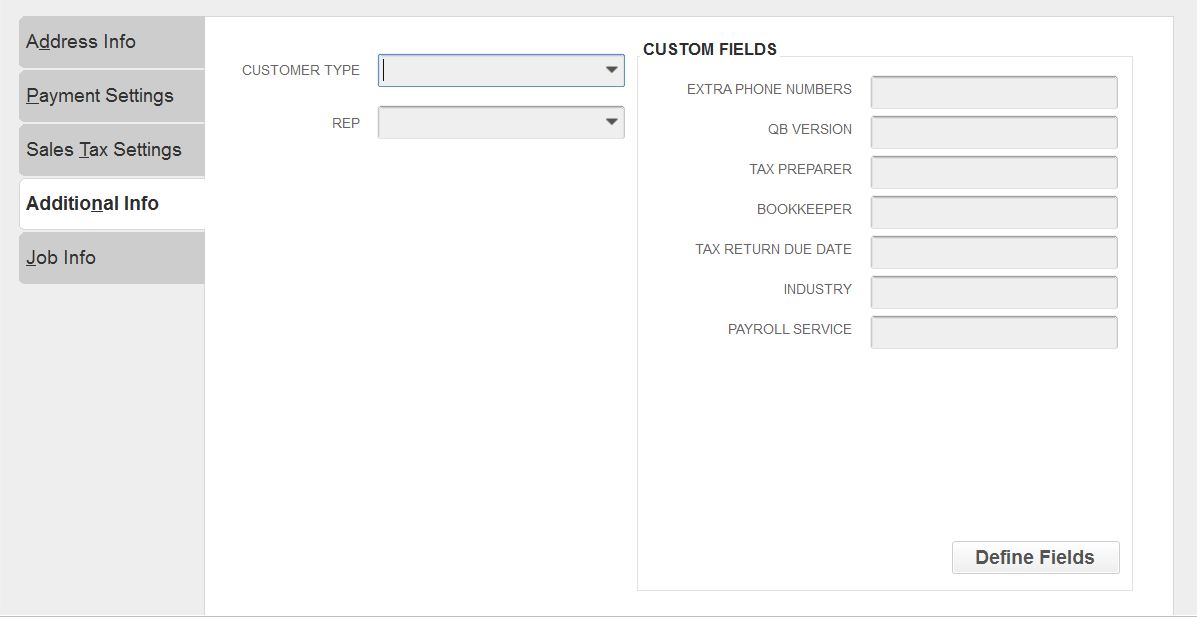

New Business Direction LLC Custom fields in your accounting software are data fields that you can define yourself. They are typically associated with customers, vendors, employees, and items, and they can help you store and categorize additional information about these stakeholders and your products and services in your business.

Custom fields in your accounting software are data fields that you can define yourself. They are typically associated with customers, vendors, employees, and items, and they can help you store and categorize additional information about these stakeholders and your products and services in your business.

Custom Fields in QuickBooks Desktop

An example custom field that can be associated with customers is their anniversary date with you. You could also decide to store their birthday, their spouse’s name, their favorite color, or their shoe size.

Custom fields add functionality to your accounting system. Here are a few examples of practical uses for custom fields:

- Contact for customer – if customers are assigned a particular team member, you can add their name in a custom field

- Frequency of service – daily, weekly, monthly

- Warehouse location

- Type of customer; for example, non-profit, construction, retail, restaurant

- Referral Source

- Preferred method of contact: email, phone, fax, text, chat

- License number

Our customer custom fields track which version of QuickBooks you use, what payroll service is active, who your tax preparer is, etc. Then we can sort on any one of these fields.

Some software allows you to choose the type of custom field you want to add. In some cases, this allows for cleaner data as the data can be limited to a certain type or certain values upon entry. Here are the most common types:

- Free form text – this is the default type; it can come as a single line or paragraph

- Check box – choose one or more values from a limited number of choices

- Radio button – choose only one value from a limited number of choices

- Drop down – choose a value from a dropdown list

- File upload – add an attachment

- Image upload – upload an image that will be displayed

- Date/time – enter a date or time

- Number – enter a number; it can be currency, integer, or another mathematical type of number

Custom fields allow you to meet your company’s unique needs over and above what the software provides by default. It’s a great way to make your data more meaningful. If you have some ideas for custom fields in your accounting software and want help setting them up, feel free to give us a call anytime.

If you want to swap services with a vendor or customer, great! But did you know barter transactions are taxable, and they need to be recorded on your books. Here’s a video from Rhonda on exactly how to record barter transactions: https://www.youtube.com/watch?v=iOAaOrojGhI

A great way to make a wonderful start to 2020 is to wrap up 2019 feeling organized and on top of the world. Here’s a checklist of items that you can start on now to make your year-end close go smoother than ever before. And don’t worry if you don’t know how to do some of these tasks – that’s what we’re here for.

A great way to make a wonderful start to 2020 is to wrap up 2019 feeling organized and on top of the world. Here’s a checklist of items that you can start on now to make your year-end close go smoother than ever before. And don’t worry if you don’t know how to do some of these tasks – that’s what we’re here for.

- Catch up on your books, especially if you do them only once a year. By doing it now, you’ll be

able to get into your accountant faster this time of year and they will appreciate getting the work done ahead of their crunch time.

able to get into your accountant faster this time of year and they will appreciate getting the work done ahead of their crunch time. - Catch up on bank reconciliations in case they are not up to date. Don’t forget your savings accounts, PayPal, and any other cash equivalents. Void any old uncleared checks if needed.

- Review unpaid invoices in accounts receivable and get aggressive about collecting them, especially if you are a cash basis tax payer. Clean up any items that are incorrect so that the account reconciles.

- Write off any invoices that are no longer collectible.

- Ask employees and vendors to update their addresses in your payroll system so that W-2s and 1099s will reflect the correct addresses.

- Collect any W-9s that you don’t already have on file for contractors that will receive a 1099 form from you.

- Collect workers compensation proof of insurance certificates from contractors so you won’t have to pay workers comp on payments you have made to them.

- Collect sales tax exemption certificates from any vendor who has not paid sales tax.

- Decide if you’ll pay employee bonuses prior to year-end. Reminder: This payroll is subject to withholding taxes.

- Review employee PTO and vacation time and reset or rollover the days in your payroll system.

- After the final payroll runs, contact your payroll software company to make any W-2 adjustments necessary for things like health insurance.

- Set the date to take inventory, and once you have, make adjustments to your books as necessary.

- Write off any inventory that is unsalable. If possible, sell scrap inventory or other waste components.

- Prepare a fixed assets register, calculate depreciation, and make book adjustments as needed. Leave the calculations and adjustments to us or your tax preparer.

- Record all bills due through year-end, and reconcile your accounts payable balance to these open bills.

- Make loan adjustments to reflect interest and principal allocations.

- Perform account analysis on all other balance sheet accounts to make sure all balances are correct and current.

- Make any additional accrual entries needed, or if you’re a cash basis taxpayer, make those adjustments as needed. You can leave these entries to your tax preparer.

- Get an idea of what your profit number will be. Choose whether you want to maximize deductions to save on taxes or whether to want to reflect more income. Decide what you can defer into 2020 or what you want to have as part of your 2019 results.

- Match all transactions with their corresponding documents – receipts, bills, packing slips, etc. – to make sure you have the paper trail you need. Go paperless – digitize these documents!

- Download your bank statements and store them in a safe place.

- Download any payroll reports and store them in a safe place.

- Scan in paper documents so that they’re stored electronically.

- File any important papers such as new leases, asset purchases, employee hiring contracts and other business contracts.

- Prepare a revenue and profit plan for 2020 and enter it into your accounting system.

- Take a look at the 2020 calendar to determine which holidays you’ll close and you’re your employees a copy of the schedule.

- Review your product and service prices if this is the time of year you do that and make any changes you decide on.

- Update your payroll system for any new unemployment insurance percentages received in a letter each year.

- Update the mileage deduction rate if that rate has changed at the beginning of the year.

- Set a time with your accountant to go over 2019 results and get ideas on how to meet your financial goals in 2020.

- Review the metrics you’ve been using in 2019 and decide on the list of metrics and corresponding values that will take you through 2020.

- Celebrate the new year; it’s a wonderful time to gain perspective and be hopeful about the upcoming year.

Start 2020 with a bang and this year-end checklist, and feel free to reach out if we can help with anything.

Learn how to back up your QuickBooks file with Rhonda Rosand, CPA of New Business Directions, LLC.

When you pay a bill in your business, are you 100 percent comfortable that the bill payment is correct and justified? Is there ever a chance that that bill is fake or fraudulent? What about duplicates? With so many fake bills being mailed to businesses these days, it makes sense to think about controls you can put into place to reduce the risk that you might write a check out of your hard-earned profits that should never be written.

When you pay a bill in your business, are you 100 percent comfortable that the bill payment is correct and justified? Is there ever a chance that that bill is fake or fraudulent? What about duplicates? With so many fake bills being mailed to businesses these days, it makes sense to think about controls you can put into place to reduce the risk that you might write a check out of your hard-earned profits that should never be written.

Accounts Payable Controls

In the accounting profession, the term “internal controls” refers to processes, procedures, and automations you can put into place to reduce errors. In accounts payable, there is a specific subset of rules and controls you can put into place to reduce risk in this area. Here are just a few ideas.

1. Approvals

All bills should be approved by the appropriate level of employee in your business. Sometimes a bill gets approved that is fake or shouldn’t be approved, especially in areas where the approver doesn’t have technical knowledge of what they are buying. Be sure to read the fine print on the bill and make sure you know what you are paying for. There are ways to streamline the approvals process.

2. Segregation of duties

The person who pays the bill should be different from the person who submitted the bill. These people should be different from the one who signs the check. This reduces employee fraud.

3. Receipt confirmation

A packing slip or other confirmation of receipt of the goods or services should be matched to the bill, line item by line item.

4. Math check

A prudent step is to check a bill’s math, at least for reasonableness.

5. Duplicate payments

If a vendor emails their bill as well as mails a hard copy, controls should be put in place (usually automated) to avoid duplicate payments on the same bill.

6. Reconciliation

If there are a significant number of transactions between you and a vendor, an accounts payable reconciliation should be performed each month via a statement.

7. Missing check numbers

7. Missing check numbers

Most systems provide a missing check numbers report that you can use to make sure all checks are accounted for.

8. Bank reconciliation

A bank reconciliation is a sure way to see exactly what checks cleared your bank account.

9. Coding

Coding each transaction to the correct expense account, inventory, asset, or cost of goods sold account is an essential part of the process.

10. Income statement review

Each month, a review of the balances in your expense accounts as well as a disbursements ledger review for reasonableness can provide added peace of mind.

11. Purchase order

Requiring purchase orders is another control you can add to your process. Purchase orders should be matched to packing slips and bills before payment or approvals are made.

12. In-depth knowledge of your business’s numbers

The more you get to know the numbers in your business, the greater chance you’ll have of accurate accounts payable handling.

If you’d like to discuss your accounts payable function with us and how it can be improved and streamlined, we’re happy for you to reach out any time.

Have a receivable you can’t collect on? Learn how to write off a bad debt in QuickBooks with Rhonda Rosand, CPA, Advanced Certified QuickBooks Proadvisor of New Business Directions, LLC.

If you want to create more revenues in your business, you need to create more transactions. Run these figures with your business to see how you can generate more revenue. Learn How Revenues Are Transactional with Rhonda Rosand, CPA, and Advanced Certified QuickBooks® Pro Advisor of New Business Directions, LLC.

The account on your income statement called Cost of Goods Sold can be confusing to non-accountants. In this article, we’ll attempt to de-mystify it and explain how it works.

The account on your income statement called Cost of Goods Sold can be confusing to non-accountants. In this article, we’ll attempt to de-mystify it and explain how it works.

Cost of Goods Sold is an account in your Chart of Accounts that is a very special type of expense. It is the amount of direct costs of items that were sold by the company. It is related to inventory, and it helps to see the flow of transactions to understand the big picture.

When you purchase an inventory item for sale, it’s considered an asset (not an expense yet) in your company. When you sell an inventory item, the asset is reduced and the Cost of Goods Sold account is increased, moving the item from an asset to an expense. It’s no longer an asset once it’s sold, and the cost of the item sold reduces your profit and is expensed into the Cost of Goods Sold account.

Some accountants will abbreviate the Cost of Goods Sold account to COGS, and you might hear them call it that.

In the case of wholesale and retail businesses, the cost of goods sold is the amount that was paid for the inventory items to be sold. In the case of a manufacturer, the costs can include the cost of raw materials, labor to produce the item, and sometimes additional allocations of other related costs. Construction businesses may have a Cost of Construction account or Contract Costs instead of COGS. Service businesses will typically not have a balance in the Cost of Goods Sold account. If they do have direct costs, the costs are often coded to a Supplies account under expenses or they have direct labor costs.

At any point in time, the cost of items you purchase are in two different accounts:

-

- The unsold items are reflected in the asset account, Inventory, on your Balance Sheet report.

- The sold items are reflected in the Cost of Goods Sold account, on your Income Statement report.

It’s important that the Cost of Goods Sold balance is accurate, because there are many good things you can learn from it when you compare it with inventory. You can learn how fast your inventory is selling, and you can determine your gross profit margin.

If your inventory purchases have been coded correctly, you can take inventory and arrive at the correct cost of unsold items. If your physical inventory does not match your books, we can help you find out why and can make a correcting entry between Cost of Goods Sold and the Inventory account so that both of them are accurate.

If you have further questions about the Cost of Goods Sold account, feel free to reach out any time.

Each month, your accounting system yields actionable information for you to run your business better. Here are some key reports that all business owners should review every month.

Balance Sheet

Balance Sheet

A quick review of the balance sheet can tell you the balances of your current assets and current liabilities. Current assets should always be larger than current liabilities; if it’s not, you may have liquidity issues.

You can also take a look at these accounts: cash, accounts receivable, and accounts payable. They should look reasonable to you based on your business history.

Accounts Receivable Aging

Your aging report can alert you to who has not paid their invoice, so that you can take action to collect that money. Any balances over 30 days should trigger a collection process since the older the receivable gets, the less likely it is to collect.

Accounts Payable Aging

Hopefully, this report is clean and you are able to pay all of your bills on time. If you have an unusually large amount in this account, you’ll want to make sure you have the future cash to pay the bills.

Income Statement

Income Statement

The first number most entrepreneurs look at on the income statement is profit. It’s a good idea to review every account balance on this report to see if it is what you expected. Some questions to ask yourself include:

- Did I generate the amount of revenue that I expected? If not, should I ramp up marketing for the next few months?

- Do all of my expenses look reasonable? Are there any numbers that look too high?

- Are my payroll expenses in line with what I was expecting?

- Which accounts caused me to generate more or less profit?

- What I can I do next month to improve performance and increase profit?

Sales Reports

There are many excellent sales reports to dive deeper into your revenue so you can see what sold and what didn’t. Sales by Item and Sales by Customer are two good options for you to get more detail about your revenue balances. By analyzing your revenue, you can see what promotions worked and how you might take action to increase sales.

These five reports are very basic, but they are also very key to your business. To profit from these reports, it’s up to you to take action in your business to improve your success.

When you purchase a new vehicle, you get the fun of riding around in a new car with the new car smell! Our job has just begun – to get your new asset recorded properly on your books. We thought it’d be fun to give you a behind-the-scenes sneak peek at our part.

When you purchase a new vehicle, you get the fun of riding around in a new car with the new car smell! Our job has just begun – to get your new asset recorded properly on your books. We thought it’d be fun to give you a behind-the-scenes sneak peek at our part.

Sales Contract

The first thing we’ll ask you for is the sales contract. It will give us the payment price of your car, and we’ll use that number to record your new asset on your balance sheet. If you paid cash with no trade-in, the journal entry we’ll make is:

| Debit: 2019 Toyota RAV4 | $25,500 |

| Credit: Cash | $25,500 |

Then we’ll decide on a depreciation method and book depreciation monthly or at year-end.

| Debit: Depreciation Expense | $5,100 |

| Credit: Accumulated Depreciation | $5,100 |

Trade-in

If you traded in a vehicle that is on your books, we’ll need to make an adjustment for that. Effectively, your old car will be eliminated from your balance sheet. If this asset had a book value and it was not fully depreciated, the net value would be compared to the trade-in value and a gain or loss on the asset sale would be recorded on your income statement.

Let’s say the balance sheet value of the three-year-old car you traded in was $10,000 ($25,000 original cost less $15,000 accumulated depreciation) and you got $8,000 on the trade-in. Here’s what we would record:

| Debit: 2019 Toyota RAV4 | $25,500 |

| Debit: Accumulated Depreciation | $15,000 |

| Debit: Loss on Sale of 2016 Car | $ 2,000 |

| Credit: Old 2016 Toyota RAV4 | $25,000 |

| Credit: Cash | $17,500 ($25,500 – $8,000 trade-in) |

We’d also start the depreciation for the new car.

New Car Loan

Most often, a new car purchase will be financed, so we have a new liability to record too. We’ll need to get a copy of the loan documents from you and an amortization schedule of the payments. Let’s say you made a ten percent down payment with no trade-in. Here’s how that would look:

| Debit: 2019 Toyota RAV4 | $25,500 |

| Credit: Cash | $2,550 |

| Credit: Toyota Loan | $22,950 |

Then, each time you make a monthly payment, the amount will need to be split between principal and interest and those amounts will need to change each month according to the amortization schedule.

| Debit: Interest Expense | $390 |

| Debit: Toyota Loan | $60 |

| Credit: Cash | $450 |

We left out a few trade secrets just to keep it intriguing. There are a lot of other numbers on a car purchase: taxes, licenses, warranties, add-ons, fees, and more. Some of these can be directly expensed, while others need to be included in the value of the asset. So if you’re happy that we’ll take care of this for you, we’re happy to do so.

Let us know if you purchase an asset this summer so we can get it booked right for you.