New Business Direction LLC

New Business Direction LLCHow to Back Up Your QuickBooks File Learn how to back up your QuickBooks file with Rhonda Rosand, CPA of New Business Directions, LLC.

Increasing your profits might sound like it’s an unattainable dream just out of your reach. But there are a finite number of ways that profits can be increased. Once you understand what they are, you’ll have clarity on how to best reach your goals.

There are two primary ways to increase profits:

- Raise revenue

- Lower expenses

That’s not particularly enlightening or instructional, is it? Let’s look at the four ways you can increase revenues and the four ways you can reduce expenses to get clearer on what actions we can take.

Four Ways to Increase Revenue

1. Raise prices

The easiest way to raise revenue is to simply raise prices. However, this is not foolproof and assumes you’ll be able to maintain the volume of sales you’ve achieved in the past.

This method is also limited by market demand, what your customers are willing to pay.

2. Add new customers

Adding new customers is what most entrepreneurs think about when raising revenue. Increasing your marketing or adding new marketing methods is typically the way to add new customers.

Another related option is to work hard to keep the customers you already have. You can also potentially contact the customers you lost and ask them to come back.

3. Introduce new products or services

For some companies, your products and services are changing every year. For others, not so much. To increase revenue, consider adding new products or services that will bring in an additional revenue stream that you didn’t have before.

Even if your products are changing every year, you can consider adding something completely different that your customer base would love. For example, a hair salon could add a nail desk, a clothing store could add handbags or shoes, a grocery store could add a coffee bar, a restaurant could add catering, a landscaper could add hardscaping, and so on.

4. Acquisition

The final way a business can increase revenue is to acquire another business in a merger or acquisition.

Four Ways to Reduce Expenses

1. Negotiate for a better deal with vendors

If you’ve been working with a vendor for a while, you may be able to re-negotiate your contract with them. This is especially common with telecom companies. Call your phone provider and ask them for the latest deal. They always favor new customers over long term customers, but they don’t want to lose customers either. Just calling them usually yields a better price than what you are paying now.

2. Change vendors

If a vendor has gotten too expensive, it might be time to look for a new vendor. Health care insurance seems to be in this category. Often, changing providers will lower your costs.

3. Cut headcount

If there is not enough work to support your employees or not enough cash flow to pay them, then it might be time for a layoff or restructuring. You might also consider outsourcing a function that you previously did in-house.

4. Cut the expense or reduce services

It might be your business no longer needs to spend money on an expense. Perhaps this expense has been automated. In this case, it’s an easy decision to cut the expense out entirely.

Those are the eight ways to increase profits. Which one makes the most sense in your business? Create a plan around these eight ideas to boost your profit in 2017, and let us know if we can help.

Tim Ferriss made the 4-hour workweek a popular concept in his 2007 book. But is there such a thing, and more importantly, can business owners like you and me cash in on it? As the last of the Baby Boomers approach retirement, the topic of working less while making the same or more income is popular.

Here are five ideas to help you work fewer hours while making the same or more income.

Active vs. Automatic Revenue

Some business models allow you to generate automatic revenue. Automatic revenue is revenue you can earn and leverage over time by doing something only once and not over and over again. Active revenue is earned while doing something over and over again. Showing up for a teaching job with a live audience is active revenue while producing and selling video recordings of the same teaching is automatic revenue.

A goal of a 4-hour workweek concept is to increase automatic revenue while reducing active revenue. You may have to think out of the box to do this in your industry, but the payoff can be huge.

Delegation and Outsourcing

One traditional way to move to a 4-hour workweek is to have others do the work. Hiring staff frees up your time and allows your business to become scalable. When it runs without you, it’s more salable too.

Time Batching

If you have a lot of distractions in your day, you can easily double your productivity by learning time batching, which is grouping like tasks together in a block or batch of time and getting them done. For example, if an employee interrupts you with questions multiple times a day, train them to come to you only once a day to get all their questions handled at one time. Take your calls one after the other in a group, and then stay off the phone the rest of the day. Do the same with email, social media, running errands, and all of your other tasks.

Automation and Procedures

New apps save an amazing amount of time. List all of your time-consuming chores and then find an app that helps you get them done faster. For example, a scheduling app can reduce countless emails back and forth when setting meetings and appointments. To-do list or project management software can cut down on emails among you and your staff. And apps like Zapier can connect two apps that need to share data, reducing data entry.

Leverage

The key to working less is to embrace the concept of leverage. How can you leverage the business resources around you to save time, increase staff productivity, and improve profits? It takes discipline and change, two difficult goals to accomplish. But when you do, you will be rewarded.

If you grant credit to customers, then you have a balance in accounts receivable. DSO stands for Days Sales Outstanding, and this helps you measure how fast your receivables are being converted to cash.

Here’s how to calculate it:

DSO = Accounts receivable balance / Annual net credit sales * 365.

DSO is measured in days and it represents how many days it takes to collect the customer invoice balance and convert it to cash.

Whether the DSO measure is “good” or not varies by industry as well as the terms you’ve set for your clients. If you’ve set your invoices to be due in 30 days and your DSO is 45 days or less, that’s pretty good. If you’ve set your invoices to be due in 10 days and your DSO is 60 days, then you might want to consider a more aggressive collection policy to speed up your cash flow.

Here are some tips to reduce DSO:

1. Invoice clarity.

Make sure your invoices are accurate and clear. Make it clear whom to make the check out to, where to mail it, the due date, and the amount due. All of these features should be easy to find on the invoice.

2. Consider discounts.

A common discount term is 2/10, net 30. This means the customer can take two percent off their invoice if they pay in 10 days; otherwise they owe the whole amount in 30 days. If you have customers from large companies, discounts are often required by policy to be taken and this can speed up your payments from them.

3. Consider electronic payments.

Going paperless with your invoicing as well as your payment process can speed up the entire billing cycle. Customers getting their bills earlier will also pay earlier.

What’s your DSO? If you need help calculating it, give us a call.

QuickBooks 2016 Desktop was recently released and there are a few new features that you will want to take a look at to see if it has something worth upgrading for.

Bill Tracker

The Bill Tracker is similar to the Income Tracker in the Customer Center that was released as a new feature in QuickBooks 2014 and improved with QuickBooks 2015. The Bill Tracker is located in the Vendor Center and allows a Snapshot View of Purchase Orders, Open Bills, Overdue Bills and Bills that have been paid in the last 30 days. Transactions can be managed from this area and batch actions can be taken to print or email and to close Purchase Orders and Pay Bills.

This Fiscal Year-to-Last Month

In the past, we had choices for date ranges on financial reports of This Fiscal Year or This Fiscal Year-to-Date as well as This Month or This Month-to-Date, none of which worked well for month-end reporting purposes. We now have This Fiscal Year-to-Last Month which allows us to print our financial reports as of the end of the Last Month, through which accounts are typically reconciled. This will allow us to Memorize Reports with the correct date instead of saving with a Custom Date that needs to be changed each time.

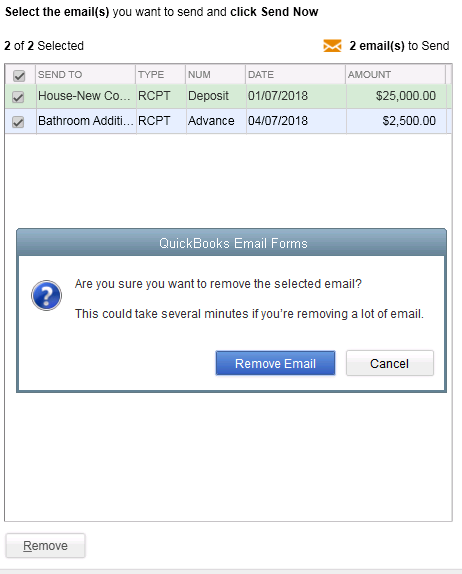

Bulk Clear “Send” Forms

Bulk Clear “Send” FormsSales Receipts, Invoices, Estimates and Purchase Orders all have an Email Later check box and it’s a “sticky” feature, meaning that once selected, it remembers for future transactions. In the past, we would accumulate many documents in the queue to be sent later and if we wished to clear the queue, it would have to be done individually. With this release, under the File menu, Send Forms, we can now Select All and click Remove.

do a Backup!

As we move into the fall season and the final quarter of the year, it’s a perfect time to commit to a project in your business that will help you reach the year’s end in better shape. Here are five ideas:

1. Back-to-School Time

If payroll expenses are one of the higher costs in your business, then it makes sense to boost your team’s productivity and maybe also your own. Fall is back-to-school time anyway, so it’s a natural time of the year to take on a course, read a business book, or hire an organizer to help you get more from your workspace.

If you spend a lot of time doing email, consider taking a course on Microsoft Outlook® or even Windows; learning a few new keystrokes could save you tons of time. If you need more time, look for a book or course on time management. Look for classes at your local community college or adult education center.

2. A Garage Sale for Your Business

Do you have inventory in your business? If so, take a look at which items are slower-moving and clear them out in a big sale. We can help you figure out what’s moving slowly, and you might even save on taxes too.

3. Celebrate Your Results

Take a checkpoint to see how your revenue and income are running compared to last year at this time. Is it time for a celebration, or is it time to hunker down and bring in some more sales before winter? With one more quarter to go, you have time to make any strategy corrections you need to at this time. Let us know if we can pull a report that shows your year-on-year financial comparison.

4. Get Ready for Year’s End

Avoid the time pressure of year’s end by getting ready early. Review your balance sheet to make sure your account balances are correct for all transactions entered to date. You will be ahead of the game by getting the bulk of the year reviewed and out of the way early.

Also make sure you have the required documentation you need from vendors and customers. One example is contract labor that you will need to issue a 1099 for; make sure you have a W-9 on file for them. If we can help you get ready for year-end, let us know.

5. Margin Mastery

If your business has multiple products and services, there may be some that are far more profitable than others. Breaking these numbers out to calculate your profit margins or contribution margins by product or service line can help you see the areas that are adding the most income to your bottom line. Correspondingly, you can determine if you have any items that are losing money; knowing will help you take the right action in your business. Refresh your financials this fall with your favorite idea of these five, or come up with your own fall project to rejuvenate your business.

contribution margins by product or service line can help you see the areas that are adding the most income to your bottom line. Correspondingly, you can determine if you have any items that are losing money; knowing will help you take the right action in your business. Refresh your financials this fall with your favorite idea of these five, or come up with your own fall project to rejuvenate your business.

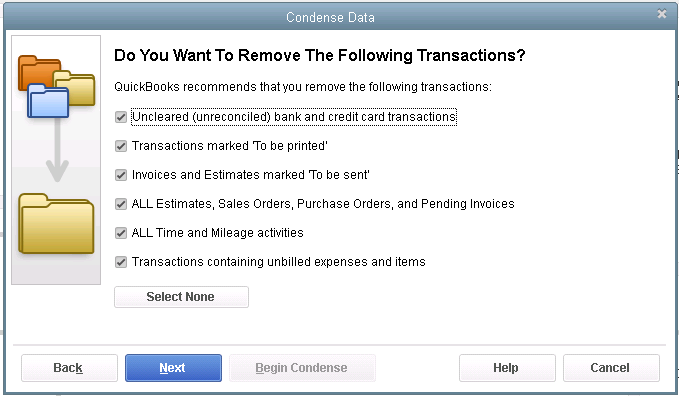

A couple of years ago, QuickBooks® gave Accounting Professionals a tool just for us – it’s only in the QuickBooks® Accountant and QuickBooks® Enterprise Accountant versions. It’s called Period Copy and it allows us to extract transactions between a set of dates for a specified period of time and condense transactions outside of the range.

This preserves transactions in the condensed file only for a particular period with entries prior to that period summarized and entries after that period removed.

This is useful for clients with file size and list limit issues as well as for third-party requests of information – not only for audit requests, but also in the event of a business sale, a divorce or legal dispute when you do not need to provide the entire QuickBooks® file.

First thing – BACKUP your data file. You are creating a new file to be issued to a third-party and you do not want to overwrite your working file.

Then under the FILE menu, UTILITIES, CONDENSE DATA –

Accept the prompt that it is ok to lose Budget data.

When it prompts you for what transactions you want to remove, select “Transactions outside of a date range” to prepare a period copy of the company file. Set your before and after dates to include the period you want to keep.

Then when it prompts you how transactions should be summarized, choose “Create one summary journal entry“.

Remove the recommended transactions.

Begin Condense.

Once complete, you will have a QuickBooks® data file with only the relevant transactions for a specific period of time and you won’t be disclosing more information than need be.

Many businesses operate with seasonal peaks and valleys. Retail stores flourish in their busy holiday season. Construction contractors are busy when the weather is good. Accountants are very busy from January through April, but also experience a quarterly peak in July and October.

Your business many have its own calendar of busy and slow times. If your business goes through slow times, then your cash flow may suffer at certain times of the year. But having seasonal sales is only one of the reasons for a bumpy cash flow.

You might also have a business where annual payments are made for many items such as equipment purchases, software licenses, insurance renewals, and other large costs. On the revenue side, it could be that your clients pay you annually, which can be hard to predict.

There are many solutions that can help to smooth out the seasonal bumps, and here are a few ideas for your consideration.

Plan for Prosperity

When income and expenses go up and down and up and down, it’s really hard to know if you have enough money for obligations coming up. Creating a budget can help a great deal. Consider creating two budgets: one that shows the ups and downs and one that averages a year’s income and expenses into twelve equal parts.

When income and expenses go up and down and up and down, it’s really hard to know if you have enough money for obligations coming up. Creating a budget can help a great deal. Consider creating two budgets: one that shows the ups and downs and one that averages a year’s income and expenses into twelve equal parts.

With both budgets, you’ll be able to see which months will be deviating from average and by how much. From there, it’s easy to create some forecasts so you can stay on top of your cash requirements.

Cash vs. Accrual Basis

It might help your business decision-making to convert your books from cash basis to accrual basis. This is a huge decision that should be made with an accounting and tax expert, as there are plenty of ramifications to discuss.

In some cases, the accrual basis of accounting will help keep those annual payments from sneaking up on you as 1/12 of the payment can be accrued on a monthly basis to a payables account. This also keeps your net income figure steadier from month to month.

If your clients prepay their accounts on a yearly basis, you can book the income monthly and keep the difference in a Prepaid account. This spreads your revenues out and recognizes them over time.

“Hiding” Money

If you feel accrual basis accounting is a little too much of a commitment, your accountant can still work with you to help you avoid the impulse of spending too much during the cash-rich busy season. Perhaps the excess cash can be put into a  savings account until it’s needed. You can draw out 1/12 each month as you need it. A little planning such as the above suggested forecasts will help you determine how much you can take out each month. You can even name the Savings account “Do Not Spend!” or “Save for a Rainy Day.”

savings account until it’s needed. You can draw out 1/12 each month as you need it. A little planning such as the above suggested forecasts will help you determine how much you can take out each month. You can even name the Savings account “Do Not Spend!” or “Save for a Rainy Day.”

If it’s just too tempting to have all that excess cash building up in the good times of the year, try one of the ideas above to take back cash flow control and smooth out those bumps.

Both the Desktop and Online versions of QuickBooks maintain an Audit Log showing a history of activity in the file by user.

QuickBooks Online Accountant allows you to see all of your QuickBooks Online accounts listed in one login screen and you can choose which client file to access.

Recently, we have witnessed several cross-overs of usernames in the Audit Logs. For example, you could be working in QuickBooks Online as yourself (the Accountant) on Client A, but the Audit Log shows you logged in as Client B on Client A’s file. If Client A happens to check the Audit Log, this could cause quite an alarm!

Unfortunately, there is nothing you can do to change the username retroactively in the Audit Log. There are, however, ways to fix this if it is happening now, and ways to prevent it from happening in the future.

If you have access to multiple QuickBooks Online companies, review the Audit Log in each company. If you log into QuickBooks Online as yourself, and the Audit Log lists another user’s name, this is where you will need to edit your Username record. To edit your username record in any of your QuickBooks Online company logins, go to https://www.login.quickbooks.com/.

Once logged in, you will see a drop-down menu of QBO companies that you have access to. After selecting the company with the incorrect username, you can edit that username to correct the issue going forward.

When you access a new QBO Company, it is always a good idea to check the Audit Log firsthand to prevent future issues.

We have notified Intuit Support of these Realm issues as have other ProAdvisors, and we are awaiting their solution. In the meantime, you may wish to reach out to your affected clients proactively.