New Business Direction LLC

New Business Direction LLCSometimes, the most telling numbers in your business are not necessarily on the monthly reports. Although the foundation of your finances revolves around the balance sheet and income statement, there are a few numbers that, when known and tracked, can make a huge impact on your business decision-making. Here are five:

1. Revenue per employee.

Even if you are a solo business owner, revenue per employee can be an interesting number. It’s easy to compute: take total revenue for the year and divide by the number of employees you had during the year. You may need to average the number in case you had turnover or adjust it for part-time employees.

Whether your number is good or bad depends on the industry you’re in as well as a host of other factors. Compare it to prior years; is the number increasing (good) or decreasing (not so good)? If it’s decreasing you might want to investigate why. It could be you have many new employees who need training so that your productivity has slipped. It could also be that revenue has declined.

2. Customer acquisition cost.

If you’ve ever watched Shark Tank®, you know that CAC is one of the most important numbers for investors. This is how much it costs you in marketing and selling costs to acquire a new client. Factors such as annual revenue, or even lifetime value of a client will affect how low or high you can allow this number to go.

3. Cash burn rate.

How fast do you go through cash? The cash burn rate calculates this for you. Compute the difference between your starting and ending cash balances and divide that number by the number of months it covers. The result is a monthly value. This is especially important for startups that have not shown a profit yet so they can figure out how much cash they need to borrow or raise to fund their venture.

4. Revenue per client.

Revenue per client is a good measure to compare from year to year. Are clients spending more or less with you, on average, than last year?

5. Customer retention.

If you are curious as to how many customers return year after year, you can compute your client retention percentage. Make a list of all the customers who paid you money last year. Then create a list of customers who have paid you this year. (You’ll need to two full years to be accurate). Merge the two lists. Count how many customers you had in the first year. Then count the customers who paid you money in both years. The formula is:

Number of customer who paid you in both years / Number of customers in the first or prior year * 100 = Customer retention rate as a percentage

New customers don’t count in this formula. You’ll be able to see what percentage of customers came back in a year. You can also modify this formula for any length of time you wish to measure.

Try any of these five metrics so you’ll gain richer financial information about your business’s performance. And as always, if we can help, be sure to reach out.

Running a small business is often about taking and managing risks. Market risks are normal but business and tax risks are another thing altogether. Most business and tax-related risks can be managed as long you know about them. Here are seven small business risks you will want to make sure are covered.

1. Best Choice of Entity

Are you operating as a corporation, limited liability company, partnership, or sole proprietor? More importantly, is the entity you are operating under providing you with the greatest tax benefits and separation from personal liability? If not, you might want to explore the alternatives to make sure you’re taking the amount of risk that’s right for you.

2. Employees or Contractors

Are your team members properly categorized when it comes to the IRS’s rules about employees versus contractors? Unfortunately, it’s not about what you and your team member decide you want. If you decide to hire contractors and the IRS determines they are employees, you could owe back payroll taxes that can cripple a small business. So you’ll want to do the right thing up front and make sure you and the IRS are in agreement, or be willing to take a future risk.

3. Insurance

If you’d like to protect yourself from possible losses through a disaster, theft, or other incident, insurance can help. There are a lot of kinds to choose from, and you’ll likely need more than one. At the minimum, make sure you’re covered by:

- Business property insurance, renters insurance, or a homeowners rider to protect your physical assets.

- Professional liability or malpractice insurance, if applicable, to protect you from professional mistakes including ones made by employees.

- Workers compensation insurance, to cover employee accidents on the job.

- Auto insurance or a non-owned policy if employees drive their car for work errands.

You may also want personal umbrella insurance, life insurance, and health insurance. Check with an insurance agent to get a comprehensive list of options.

4. Sales Tax Liability

Are you sure you’re collecting sales tax where you should be? As the states get greedier, they invent new rules for liability. For example, if one of your contractors lives in another state, you may owe sales tax on sales to customers who live there even if you don’t live there or have an office there.

Nexus is a term that describes whether you have a presence in a state for tax purposes. Having an office, an employee or contractor, or a warehouse can extend nexus so that you’d need to collect and file sales tax for those states. If you’re in doubt, check with a professional, and let us know how we can help.

5. Underpricing

Most small businesses make the mistake of underpricing their services, especially when they start out. If you started out that way, it’s awfully hard to catch up your pricing to a reasonable level. Knowing the right price to charge can make the difference between whether the company last six months or six years. You can mitigate this risk by getting cost accounting help from your accountants who can help you calculate your margins and determine if you’re covering your overhead and making a profit.

6. Legal Services

Legal services can be expensive for a small business, so sometimes owners cut corners and take risks. Attorneys are needed most when it comes to setting up your entity, reviewing contractual agreements such as leases and loan agreements, settling conflicts, advising on trademark protection, and creating documents such as terms of service, employment agreements, and privacy policies. Just one mistake on any of these documents can cost a lot, so be sure it’s worth the risk.

7. Accounting Services

Doing your own accounting and taxes can be risky if they’re done wrong or incomplete. You could end up paying more than you should if you leave out deductions you’re entitled to. Worse, if you do your books wrong, you could end up overpaying taxes without realizing it. A common bookkeeping error results in doubling sales, and while it might look good, you certainly don’t want to pay more than what’s been truly received.

How did you do with these seven risks? If you need to reduce your risks in any of the areas, feel free to reach out for our help.

Most small businesses need help with cash during certain stages of their growth. If you find that you have more plans than cash to do them with, then it might be time for a loan. Here are five steps you can take to make the loan process go smoother.

1. Make a plan.

Questions like how much you need and how much you will benefit from the cash infusion are ones you should consider. If you don’t already have some version of a budget and business plan, experts recommend you spend a bit of time drafting those items. There’s nothing worse than getting a loan and finding out you needed twice the cash to do what you wanted to accomplish.

2. Know your credit-related numbers.

Do you know your credit score? Is there anything in your credit history that needs cleaning up before it slows down the loan approval process?

Take a look also at your standard financial ratios. These are ratios like your current ratio (current assets / current liabilities) and debt-to-equity ratio. If these are in line with what your lender is expecting, then you are in good shape to proceed.

3. Research your options.

Luckily, there are many more options for financing your business today than there have been in the past. Traditional options, such as banks, still exist, but it can be difficult to get a bank loan for a small business.

Here are some online loan sources where investors are matched with borrowers via an online transaction:

- Kabbage

- OnDeck

- LendingClub

- FundBox

- BlueVine

Or you can go to Fundera and compare which loan is the most economical.

There is also crowdfunding, which is very different from a loan. Crowdfunding is a way to raise cash from many people who invest a small amount. Top sites include GoFundMe and KickStarter, where you can find out more about how it works.

Other ways to get cash include tapping into your personal assets: using credits cards, refinancing a house, and borrowing money from family and friends.

4. Create your loan package.

Most lenders will want to know your story, and a loan package can provide the information they need to decide whether they want to loan you money or not. A good loan package includes the following:

- A narrative that includes why you need the loan, how much you want, and how you will pay it back. A good narrative will also list sources of collateral and a willingness to make a personal guarantee.

- Current financial statements and supporting credit documentation, such as bank statements and credit history.

- A business plan and budget, or portions of it, that cover your business overview, vision, products and services, and market.

- A resume or biography of the business owners and a description of the organization structure and management.

While it takes time to put together a great loan package, it’s also a great learning experience to go through the exercise of pulling all of the information together.

5. Execute!

You’re now ready to get your loan. Or not. Going through these five steps helps you discover more about your business and helps you make an informed decision about whether a loan is still what you want and need.

Throughout the process, you may have learned new information that tells you you’re not quite ready for a loan, or that in fact, you are. At any rate, preparing for a loan is a great learning process, and the good news is there are lots of avenues for small businesses to get the cash they need to grow.

Spring denotes new growth, fresh starts, and spring cleaning. Why not apply these ideas to your sales so they can blossom along with spring flowers? Here are six ideas to put the spring into your sales.

1. Spring Cleaning Sales

Get rid of old inventory by having a spring sale that will clean out your closets and put some money in your account. Look through your items for sale and find the ones that haven’t moved like you expected. Mark them down and move them out.

2. New Items and Services from Customer Ideas

Now that you’ve gotten rid of the old stuff, you have room for new. If you’re not sure what your clients want or need, ask. Use Survey Monkey to find out what your clients can use. If you don’t have what they want, make it, buy it, or partner with someone who does. Then let everyone know, “based on popular demand” of course, that you have new items for sale just in time for spring.

What questions should you ask in your survey? Try questions like these to draw out your customers’ needs and wishes and to discover any shortcomings you might have not known about:

- What items/services are on your wish list that you’d like us to stock/provide?

- How do you currently use our services/products?

- What do you wish our items accomplished that they don’t now?

- How would you recommend we expand our selections?

- What do you wish we did better?

3. The Old “Fries with Your Burger” Upsell

Waitpersons offer desserts and appetizers, office supply staff offer cables and accessories with hardware purchases, and software vendors offer the next level package. Almost every business practices a form of upsell these days, so if you don’t, you’ve got a new opportunity right here.

Dust off your old upsell procedures and try these ideas to rejuvenate your upsells:

- Re-visit your inventory to pair complementary items for upsell potential.

- Retrain your staff for upsell language at the time of sale.

- Re-package like items to offer more bundles and groups.

4. New Prices

When is the last time you’ve raised your prices? If it’s been a while, then it’s a great opportunity to increase revenue with little additional effort.

5. Spread the Word with Spring Samples

Samples can help get your product or service into the hands of many potential buyers. Buyers can better experience your product and reduce their perceived risk.

Not all businesses can provide samples, but there is always the next best thing. Where your product is not consumable, you can sometimes provide a portion of the product, such as a carpet sample, wallpaper swatch, or floor tile. With retail clothing, pictures will have to do. With books or courses, you can provide a sample chapter or a demo video. And with services, case studies or proof of concept will suffice.

6. Offer a Customer Reward Program

Put together a program to reward your most loyal clients and to make them even more loyal to you. Some of the perks could include monthly gifts, priority service, an exclusive event, and/or discounts. The price can be structured as a membership fee, retainer, or package price. Increasing contact, benefits, and communication with these clients is always a good investment.

Try one of these six ideas to put the spring in your sales this season.

A 2014 Global Fraud Study conducted by the Association of Certified Fraud Examiners (ACFE) estimates that the average business loses five percent of their revenues to fraud. The global total of fraud losses is $3.7 trillion. The median fraud case goes 18 months before detection and results in a $145,000 loss. How can you avoid being a fraud victim?

The first step is to become more aware of the conditions that make fraud possible. The fraud triangle is a model that describes three components that need to be present in order for fraud to occur:

- Motivation (or Need)

- Rationalization

- Opportunity

When fewer than three legs of the triangle are present, we can deter fraud. When all three are present, fraud could occur.

Motivation

Financial pressure at home is an example of when motivation to commit fraud is present. The fraud perpetrator finds themselves in need of large amounts of cash due to any number of reasons: poor investments, gambling, a flamboyant lifestyle, need for health care funds, family requirements, or social pressure. In short, the person needs money and lots of it fast.

Rationalization

The person who commits fraud rationalizes the act in their minds:

- I’m too smart to get caught.

- I’ll put it back when my luck changes.

- The big company won’t miss it.

- I don’t like the person I’m stealing from.

- I’m entitled to it.

At some point in the process, the person who commits fraud loses their sense of right and wrong and their fear of any consequences.

Opportunity

Here’s where you as a business owner come in. If there’s a leak in your control processes, then you have created an opportunity for fraud to occur. People who handle cash, signatory authority on a bank account, or financial records with poor oversight could notice that there is an opportunity for fraud to occur with the ability to cover the act up for some time.

Seventy-seven percent of all frauds occur in one of these departments: accounting, operations, sales, executive/upper management, customer service, purchasing and finance. The banking and financial services, government and public administration, and manufacturing industries are at the highest risk for fraud cases. (Source: ACFE)

Prevention

Once you understand a little about fraud, prevention is the next step. To some degree, all three points on the triangle can be controlled; however, most fraud prevention programs focus on the third area the most: Opportunity. When you can shut down the opportunity for fraud, then you’ve gone a long way to prevent it.

While we hope fraud never happens to you, it makes good sense to take preventative steps to avoid it. Please give us a call if we can help you in any way.

Providing great service can make a huge difference in a small business. For companies like Zappos, Nordstrom, and Southwest Airlines, customer service is a differentiator from their competitors. Done right, good customer service can bring lots of referrals that lead to increased revenue. Here are five tips to improve service to your customers.

1- “Welcome Home” Greeting

Consider your business as your home and your customers as invited guests. No matter how they come to you, whether by phone, email, or in person, greet them like you would a guest. If your business has a storefront and customers walk in, have your employees greet them immediately with a welcome message that ends in “Please, make yourself at home.” If your prospect or customer calls you, greet them warmly with “I’m so glad you called.” If a customer or prospect emails you, personally email them back (no autoresponders) to let them know you received their message and when you will be replying.

A warm welcome every time your customer contacts you will make them feel important.

2- Throwback Thank You Cards

Be old-fashioned for a change and handwrite thank you cards to your top clients. You can get blank folding cards with matching envelopes from your local printer or paper shop and have your company logo printed on them. If you don’t have time for that, consider SendOutCards.com.

3- Apologize

Things are bound to go wrong. Be quick with a heartfelt apology whether it’s your fault or not. If your customer struggled with anything – your website, shopping cart, store display, out-of-stock item, and so on – teach your employees to apologize first, then own the problem and get it fixed for all future clients. You can also teach them the language, “thank you for giving us the opportunity to fix this for all future clients.”

4- Mystery Shop

Periodically hire a mystery shopper to evaluate the customer experience at your business. These customer service experts will provide you with a list of suggestions, from your initial voice mail recording to paying your bill. Everywhere your business touches a client should be streamlined, easy, and sealed with a smile.

5- Listen

Your customers can be the best source of ideas for your next new revenue stream. Listen to their feedback and incorporate their ideas into your business.

Try these customer service tips to delight your customers, and watch your revenue grow.

If you want 2016 to be better than 2015, you have to do something differently in 2016 than you did in 2015. It’s a simple but profound realization. Change brings the opportunity to make things better; it can be scary yet exciting at the same time.

Ask yourself what you are going to do differently to have your best year ever. Here are some questions and exercises to consider:

Clarify Your Vision

What does the world look like after it’s consumed your product or service? A vision statement for a company helps to keep everyone on track and seeing the bigger picture of what they’re accomplishing day after day. How is the world smarter, more beautiful, happier, healthier, or wealthier after they’ve left your business?

If you haven’t written your business vision and mission statement, consider this exercise for 2016.

Create New Habits

What habits are holding you back? Which ones are propelling you forward? Choose one habit that’s costing you the most and make a commitment to drop it from your 2016 repertoire. Conversely, identify the habit that is brining you happiness and wealth and multiply it.

Let Go

Sometimes we need to let go before we can move forward. What do you need to let go of? Are there customers or employees in your life that sap your energy or your bank account?

Build Your Support Structure

Are you short-staffed? The way you manage your time has everything to do with your success or the lack of it. If you are taking up your time with a lot of low-dollar tasks, it’s going to be hard to boost your income and get ahead. Surround yourself with support to do everything that can be delegated, including personal tasks such as grocery shopping, housekeeping, cooking, and lawn maintenance as well as tasks such as filing, bookkeeping, appointment scheduling, and routine customer service.

Make a list of areas where you could use support, and fill these gaps. In today’s world, you don’t need to hire full time people to fill these slots; you can simply get responsible contractors, other small businesses, and virtual assistants to build your support team.

Focus

What project or task would make a huge difference in 2016 if you could pull it off? Focus on the high payback projects and commit to one, even though it might be out of your comfort zone. Imagine the difference in your business once it’s completed, and get inspired to get started.

Choose just one of these areas to start your 2016 out with hope, intention, and excitement.

You may have heard that Google has rolled out a new search algorithm that ranks mobile-friendly websites higher than sites that are not mobile-friendly. You don’t need to worry too much about this unless you rely on website leads for new clients to build your business.

If you do rely on website leads for new business and your leads have dropped off over the summer, the reason could be that your site is not mobile-friendly and has been ranked lower because of it. Here are three steps you can go through to determine the status of your site.

Take a Free Mobile-Friendly Test

Go to this link and enter your domain name.

https://www.google.com/webmasters/tools/mobile-friendly/

It takes about a minute or two to find out whether your site is mobile-ready.

If your site passes, you’re done! You don’t need to do anything. If it doesn’t, then go to step 2.

Contact Your Webmaster

Ask your webmaster for an estimate to get your site mobile-ready.

Take Action

Google started making changes to the search algorithm the week of April 20, 2015 has now implemented it worldwide. To benefit from mobile traffic and a higher search ranking, make plans to get your site mobile-friendly sooner rather than later.

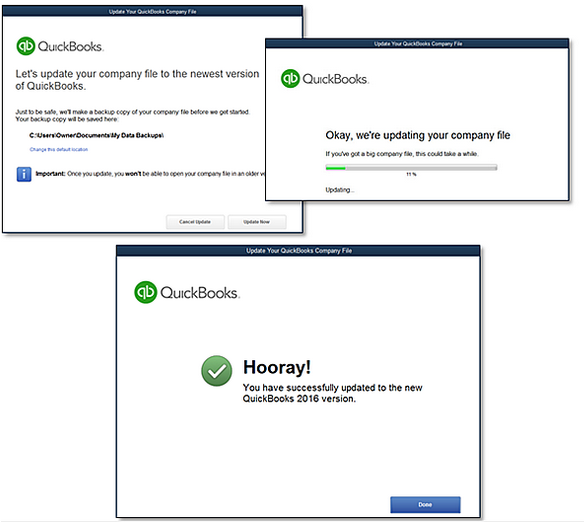

QuickBooks 2016 Desktop was recently released and there are a few new features that you will want to take a look at to see if it has something worth upgrading for.

Bill Tracker

The Bill Tracker is similar to the Income Tracker in the Customer Center that was released as a new feature in QuickBooks 2014 and improved with QuickBooks 2015. The Bill Tracker is located in the Vendor Center and allows a Snapshot View of Purchase Orders, Open Bills, Overdue Bills and Bills that have been paid in the last 30 days. Transactions can be managed from this area and batch actions can be taken to print or email and to close Purchase Orders and Pay Bills.

This Fiscal Year-to-Last Month

In the past, we had choices for date ranges on financial reports of This Fiscal Year or This Fiscal Year-to-Date as well as This Month or This Month-to-Date, none of which worked well for month-end reporting purposes. We now have This Fiscal Year-to-Last Month which allows us to print our financial reports as of the end of the Last Month, through which accounts are typically reconciled. This will allow us to Memorize Reports with the correct date instead of saving with a Custom Date that needs to be changed each time.

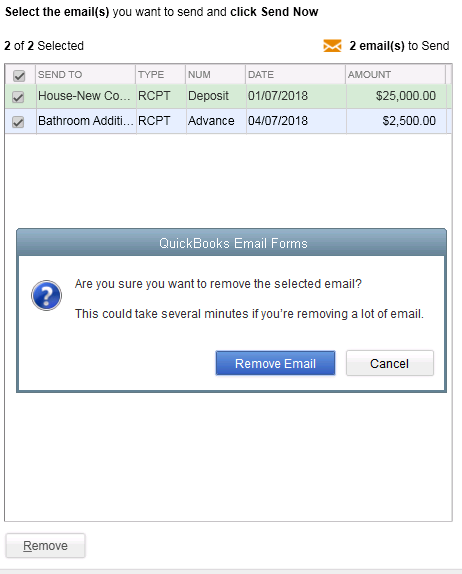

Bulk Clear “Send” Forms

Bulk Clear “Send” FormsSales Receipts, Invoices, Estimates and Purchase Orders all have an Email Later check box and it’s a “sticky” feature, meaning that once selected, it remembers for future transactions. In the past, we would accumulate many documents in the queue to be sent later and if we wished to clear the queue, it would have to be done individually. With this release, under the File menu, Send Forms, we can now Select All and click Remove.

do a Backup!