Effective December 1, 2016, federal overtime regulations will change and may affect how you are paying your employees. These overtime updates will affect 4.2 million workers across the country.

The new rules will raise the salary overtime-eligibility threshold from $455/week to $913 ($47,476 per year). This new threshold will increase every three years. Salaried workers already entitled to overtime will get increased protection.

Employers have a choice of three actions they can take to employees who become eligible for overtime that weren’t before.

- Pay time-and-a-half for overtime work.

- Raise worker’s salaries above the new threshold.

- Limit worker’s hours to 40 per week.

Let’s say you have an employee that earns $500 per week and works 50 hours a week. Previously, you didn’t pay overtime, but beginning December 1, 2016, you will need to. At $12.50 per hour, you would owe them the regular $500 plus 10 hours of overtime at $187.50.

Let’s say you have an employee earning $800 per week and they work 50 hours. Previously, you didn’t pay overtime, but now you will need to consider it. You could pay them overtime, which works out to a weekly pay of $1100. Or you can choose to give them a raise to $913 per week – the new threshold – and continue to exempt them from overtime. The latter is the lowest cost alternative.

In both cases above, it may be cheaper to hire an additional part-time worker to work the 10 extra hours per week.

You can find more about the new overtime law here:

https://www.dol.gov/featured/overtime/

And if you have any questions about your payroll, feel free to reach out anytime.

The New Business Directions Team is bringing the #1 employee-rated and requested Time Tracking Software to you. Sondra Love, Wayne Kukuruza, and Rhonda Rosand, CPA have recently joined the 6000+ TSheets PRO community by participating in an exclusive TSheets PRO certification course accredited by CPAacademy.org.So what exactly is TSheets? TSheets is a time tracking and scheduling software designed for businesses that track, manage, and report time. TSheets provides the alternative to paper timesheets and/or punch cards to simplify human resource and data processing roles for companies of all sizes.

But here’s the best part, TSheets fully integrates with QuickBooks by syncing accurate timesheets to your QuickBooks file and eliminating manual, duplicate time entries. Tracked and approved time can now be easily exported to either QuickBooks® Online or Desktop with just one click. Management can then use their favorite tools within QuickBooks to process payroll, calculate job costing, and create invoices in a more simplified work flow.

TSheets is also a scheduling software making it faster and easier to build and share schedules with employees, assign jobs, and alert shifts while increasing profitability and improving communication. In other words, we want to keep your workforce running like a well-oiled machine.

Oh, and have I mentioned their amazing customer service department? The TSheets team who’s behind the product is just as amazing as the software itself. Customer service team is passionate about their customers and provides exceptional support in times of need. They make your entire TSheets experience FUN and might even give you a smile or two.

The best cakes have layers and layers of different delicious flavors to enjoy. Stacked on top of one another, each layer is baked separately and becomes part of the whole. Like a layer cake, your business expenses have layers of meaning to them. When you can understand how expenses play a part in profit, you can manage them better.

Here’s how to make a layer cake of your business expenses. Let’s start with the most direct expenses.

Direct Costs

If you have inventory you will have a balance in the Cost of Goods Sold account. It should represent how much you paid for product or inventory that you are selling. It is the most direct expense of all the expenses; if you don’t spend this money, you would not have a product.

If you sell services, you should not have a balance in Cost of Goods Sold, but you will have direct expenses that are tied to performing your services. These might include labor from wages of the employees who carry out the services for clients. Any supplies directly involved with delivering services should be included as well.

You may also have other direct costs related to selling specific products or to servicing specific accounts.

Indirect Costs

The next layer includes indirect expenses. These expenses do not make up your product directly and might contribute to several different lines of products. Indirect costs might be attributable to a group of products or projects and can be apportioned accordingly.

Overhead

Although overhead is technically a form of indirect cost, it’s good to create a separate layer for it. It includes management salaries, rent, utilities, and other fixed costs that cannot be directly allocated to a product or service.

Assembling the Layers

A wonderful exercise is to classify each of your expense accounts in your Chart of Accounts as direct, indirect, or overhead. In that way, you can see how each account contributes to the costs of running your business. Some questions to ask yourself:

- What is my gross margin before indirect costs and overhead?

- What is my gross profit after indirect costs and before overhead costs?

- How can I cut down on any of these categories of expense?

- What is my breakeven volume in sales before overhead is factored in?

- Can my profit margin be changed if I spent less in a certain area?

This layered view is just another way to view the financial aspects of your business and can help you make better decisions down the road.

You can also break the layers down even further by classifying the expenses as critical and non-critical. This will help you determine where best to invest while maintaining the level of profit you desire.

You can’t manage what you don’t measure. Layering your expenses will help you have your cake and eat it too. And if we can help, just reach out as always.

This year’s theme was “epic” designed as the epic conference to empower small business advisors to develop and sustain the epic practice that distinguishes itself and embraces the key differences that separate ProAdvisors around the good, the great and the “epic.”

Sessions

The four-day conference kicked off each morning with Power Breakfast Sessions followed by main stage presentations with keynote speakers such as Daymond John of Shark Tank, Joe Buissink of Canon Explorer of Light, and author Mike Michalowicz of Profit First. In between general session, attendees dispersed around the conference center into rooms where cutting edge training sessions were being held. Training sessions were broken down into 5-tracks for Practice and Professional Development, Practice Growth, In-Depth QuickBooks Training, ProAdvisor Certification Training and QB Integrated Apps.

If you were fortunate enough to attend, Rhonda Rosand, CPA taught a 100-minute informative training session titled Successful Implementations from Initial Contact through Ongoing Support on Sunday, May 22nd. As the evenings came around, networking sessions were held consisting of ICB Bookkeeper’s Symposium, the Woodard Network Social hosted within Atlantis’ stunning marine life exhibit, The Dig and of course, the infamous TSheets dance Party on TSheets Tuesday.

taught a 100-minute informative training session titled Successful Implementations from Initial Contact through Ongoing Support on Sunday, May 22nd. As the evenings came around, networking sessions were held consisting of ICB Bookkeeper’s Symposium, the Woodard Network Social hosted within Atlantis’ stunning marine life exhibit, The Dig and of course, the infamous TSheets dance Party on TSheets Tuesday.

Sondra’s Take on Vendors

In between training, I was able to visit the exhibit ballroom which held over 90 vendors, some of which were very familiar. I came across software I use everyday to make my work flow run smoothly and now I am able to put a face to the product. For example, SmartVault allows me to access files anywhere, anytime and from any device. I also have the capability to securely share files with clients and our team.

In between training, I was able to visit the exhibit ballroom which held over 90 vendors, some of which were very familiar. I came across software I use everyday to make my work flow run smoothly and now I am able to put a face to the product. For example, SmartVault allows me to access files anywhere, anytime and from any device. I also have the capability to securely share files with clients and our team.While at Scaling New Heights, I learned the importance of technology and how it relates to strengthening our firm and supporting our clients.

Two very important skills for entrepreneurs to master are marketing and finances. Combine them by understanding the numbers behind marketing, and you have an even more powerful understanding of exactly what makes your business tick.

Key Numbers – Cost Per Client Acquisition

Do you know how much it costs your business to bring in one client? The technical term is “Cost per customer acquisition,” and it’s computed by adding the total marketing and sales costs excluding retention costs and dividing them by the total number of clients acquired during a period of time.

Cost per customer acquisition is important to know because then you can compute how long it takes before your business begins to make a profit on any one customer. In software application services with a monthly fee, the breakeven for a client can be around ten months.

It’s essential to understand this dynamic for pricing and volume planning purposes. If your services or products are priced too low so that your acquisition costs are not recouped in a reasonable period of time, it can play havoc with your cash flow as well as your profits. If you don’t have enough volume to cover overhead and acquisition costs, then your company will be in trouble in the long term.

Customer Lifetime Value

There is a simple and an academic formula for customer lifetime value. You can estimate it by multiplying the average sale of a customer by the average number of visits per year by the number of years they remain a customer. That’s the easy version.

The more difficult version of this formula takes into account retention rates and gross profit margins. The formula is: Average customer sales for life times the gross profit margin divided by the annual churn rate.

Once you know and track these numbers in your business, you’ll be better able to make smart decisions about your marketing investments and your pricing. And if we can help you, please reach out as always.

It’s not hard to see when your home needs a good cleaning but QuickBooks company file errors are harder to recognize so here are a few errors to watch for:

- Performance problems

- Inability to execute specific processes

- Occasional program crashes

- Missing data (accounts, names, dates)

- Refusal to complete transactions

- Mistakes in reports

One thing you can do on your own is to start practicing good preventive medicine to keep your QuickBooks company file healthy. Once a month or so, perhaps at the same time you reconcile your bank accounts, do a manual check of your major Lists.

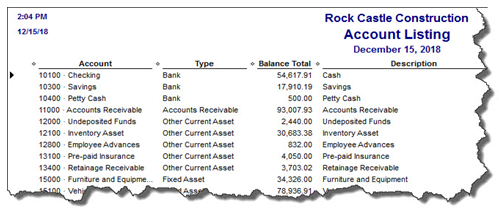

Run the Account Listing report (Lists, Chart of Accounts, and Reports). Ask yourself: Are all of your bank accounts still active? Do you see accounts that you no longer use or which duplicate each other? You may be able to make them inactive or merge duplicates. Be very careful here. If there’s any doubt, leave them there. Do not try to fix the Chart of Accounts on your own. Let us help or speak with your tax preparer. Do not make accounts with balances inactive.

Figure 2: You might run this report periodically to see if it can be abbreviated.

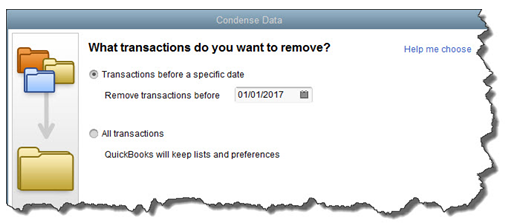

A Risky Utility

The program’s documentation for this utility contains a list of warnings and preparation steps a mile long. We recommend that you do not use this tool. Same goes for Verify Data and Rebuild Data in the Utilities menu. If you lose a significant amount of company data, you can also lose your company file. It’s happened to numerous businesses.

Figure 3: Yes, QuickBooks allows you to use this tool on your own. But if you really want to preserve the integrity of your data, let us help.

The best thing you can do if you notice problems like this cropping up in QuickBooks – especially if you’re experiencing multiple ones – is to contact us. We understand the file structure of QuickBooks company data, and we have access to tools that you don’t. We can analyze your file and take steps to correct the problem(s).

Your copy of QuickBooks may be misbehaving because it’s unable to handle the depth and complexity of your company. It may be time to upgrade. If you’re using QuickBooks Pro, consider a move up to Premier. And if Premier isn’t cutting it anymore, consider QuickBooks Enterprise Solutions.

There’s cost involved, of course, but you may already be losing money by losing time because of your version’s limitations. All editions of QuickBooks look and work similarly, so your learning curve will be minimal.

We Are Here for You

We’ve suggested many times that you should contact us for help with your spring cleanup. While that may seem self-serving, remember that it takes us a lot less time and money to take preventive steps with your QuickBooks company file than to troubleshoot a broken one.

Outsmart your accountant and other financial friends with these accounting-related definitions:

Fiscal Year

Most companies report their results on a calendar year, from January 1 through December 31. Some companies use a different year for reporting, and that’s called a fiscal year. For example, Intuit’s fiscal year runs from August 1 to July 31. A nonprofit commonly runs from July 1 to June 30.

The word fiscal alone refers to government or public revenues and expenditures. A fiscal year can also be considered the period where companies report their financial results to the public.

Budget

Most companies sit down once a year and plan what they intend to spend. This set of numbers is a budget. It is prepared in income statement format which includes planned revenue and expenses. It can be done for a year, monthly or both.

A common report that compares budget to actual figures is the Income Statement Comparison to Budget which includes columns for month and year-to-date actual, budget, and variance (the difference).

Forecast

While a budget is a longer term plan, a forecast is an attempt to predict the short-term future. Forecasts can be made for cash flow, predicting your bank account balance, or can be focused on potential profit for a period. A forecast is created by enumerating current and expected short-term cash commitments.

General Ledger

A general ledger is a fancy word for your accounting books. It’s also a very specific report that lists each account within the chart of accounts, beginning balances, the activity of each account for a particular period of time, and ending balances. It includes both balance sheet accounts, such as cash, accounts receivable, and accounts payable, and income statement accounts, such as revenue and expenses.

Fixed Asset

A fixed asset is a special type of asset that includes items such as land, vehicles, furniture, buildings, office equipment, plants, and machinery. Fixed assets cannot easily be converted into cash (cash equivalents are termed current assets) and they must last longer than one year. They are physical or tangible (as opposed to intangibles such as patents and trademarks).

Depreciation

Most fixed assets except land depreciate in value over time. For example, when you drive a new car out of the lot, no one will give you what you just paid for it. This reduction in value over time is recognized on accounting books by recording depreciation. Since assets need to be recognized at market value, depreciation is an estimate of this adjustment. Depreciation becomes an expense and reduces the value of the fixed asset. Unlike most other transactions, cash is not affected when recording depreciation.

Accrual

There are two ways to keep books when it comes to the timing of how items are recorded: the cash method and the accrual method. Let’s invoke Popeye the Sailor Man’s friend Wimpy who always says, “I’ll gladly pay you Tuesday for a hamburger today.” Let’s say today is the Friday before this famous Tuesday.

If you are using the cash basis method, you would record the entire transaction on Tuesday, when you get the cold hard cash. If you are using the accrual basis, you would have two entries: one on Friday to record the sale to accounts receivable and one on Tuesday to zero out the receivable and increase cash. It’s the same net, effect; the only difference is in the timing.

Most small businesses that extend credit keep their books on an accrual basis so they can keep track of everything. Most taxes are paid on cash-basis books, requiring adjusting entries at year end that reverse at the beginning of the year.

Balance Sheet

A balance sheet is a very common report of all of the business’s account balances as of a specific date, such as December 31. These accounts include cash, receivables, fixed assets, liabilities, equity and others.

Journal Entry

A journal entry is usually an adjustment that is made to the accounting books. The result is that some accounts increase and others decrease. In theory, every transaction made to a company’s books is a journal entry. When you write a check and it’s cashed, cash goes down and an expense is increased. When you receive a payment, cash goes up and revenue goes up. Each of these transactions is a journal entry.

Do you feel a bit smarter? I’m not sure how exciting this is for cocktail table talk, but hopefully you feel smarter when it comes you’re your business’s accounting function.

The New Business Directions team is pleased to announce our newest QuickBooks® Online ProAdvisor!

Sondra Love has successfully completed the requirements to earn her QuickBooks® Online  2016 certification. This training will allow Sondra to provide assistance to businesses setting up, navigating and troubleshooting their QuickBooks® Online software.

2016 certification. This training will allow Sondra to provide assistance to businesses setting up, navigating and troubleshooting their QuickBooks® Online software.

New Business Directions, LLC specializes in QuickBooks® consulting and training services, coaching small business owners, and providing innovative business solutions.

To learn more about New Business Directions, LLC and QuickBooks®, please call (603) 356-2914 to schedule an appointment or visit our website.

Rhonda Rosand, CPA has successfully completed the requirements to earn her designation for the twelfth consecutive year as a Certified QuickBooks® ProAdvisor.

Rhonda Rosand, CPA has successfully completed the requirements to earn her designation for the twelfth consecutive year as a Certified QuickBooks® ProAdvisor.

Certified QuickBooks® ProAdvisors are CPA’s, accountants and other professionals who have completed comprehensive QuickBooks® training courses and met the annual testing requirements in order to become certified as experts in QuickBooks®. The courses are designed for accounting professionals and consultants who have a solid understanding of accounting principles.

An accounting professional since 1986 and a Certified Public Accountant since 1992, Rhonda is a one-of-a-kind, live-your-dreams business coach and trainer. She has real-world business experience, well-honed problem-solving skills and an enthusiastic, energetic, can-do attitude. She believes that a successful business stays that way not only by managing its finances well, but also through a proactive plan that includes marketing, strong customer service and long range planning. “Today it is not enough to have a good advisor who works with you once a year”, says Rosand. “The best approach is to actively manage all aspects of your business, all year long.”

Rhonda Rosand, CPA is the owner of New Business Directions, LLC.She specializes in QuickBooks® consulting and training services, coaching small business owners and providing innovative business solutions.

To learn more about New Business Directions, LLC and QuickBooks®, or to schedule an appointment, please call (603)356-2914, email rhonda@newbusinessdirections.com or visit the website at www.newbusinessdirections.com.

QuickBooks 2016 offers some new features that we are excited to share with our fellow accounting professionals. Batch Delete/Void Transactions and enhanced Statement Writer Support are two of the latest features available to Accountants only. Sorting on Item Custom Fields and Auto Copy Ship to Addresses are features only available in Premier (including Accountant) and Enterprise versions of the software.

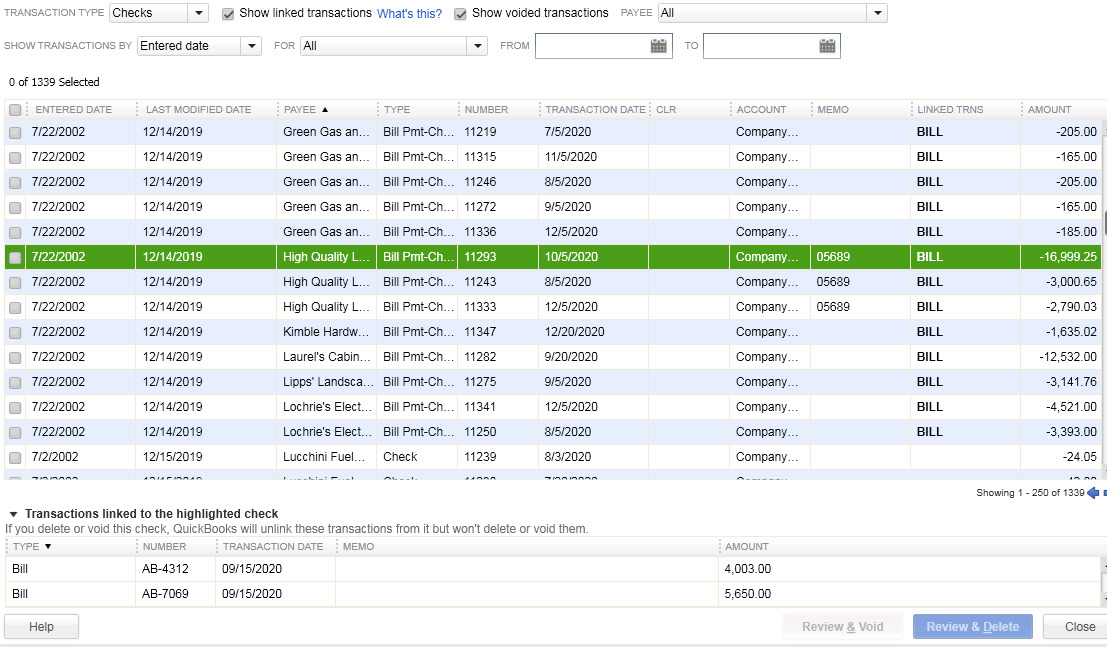

Batch Delete/Void Transactions

We are cautiously excited about this new feature as it could prove to be quite dangerous in the wrong hands. Fortunately, Intuit realized that and only made the tool available in the Accountant and Enterprise versions of the software and in the Accountant Toolbox in the Pro and Premier versions.

It works for Invoices, Bill and Check transactions, but not for Credit Cards Charges or Deposits, at this time. It is also not available for Payroll or Sales Tax Transactions. The columns can be sorted by Entered Date, Modified Date or Transaction Date as well as by Payee, Type, Number, Account or Amount.

Any other transactions that are linked to the transaction to be voided/deleted are highlighted for you to be aware and to address them as well, if need be. For example, voiding a Bill-Check does not void the related Bill.

I am hopeful that Intuit will improve this feature and add the ability to work with Credit Card Charges, as I have seen many occasions where these were imported to the wrong account or even twice to the same account. As with any tool of this nature, we recommend a backup before and to Void instead of Delete.

Statement Writer Support for Microsoft Office

I do not prepare financial statements, but for those who do and for those who use the QuickBooks Statement Writer, it is essential to have the integration with Microsoft Word and Excel. With QuickBooks 2016, we have this integration with the Accountant and Enterprise versions of the software. However, we still do not have support for the cloud-based Microsoft Office 365.

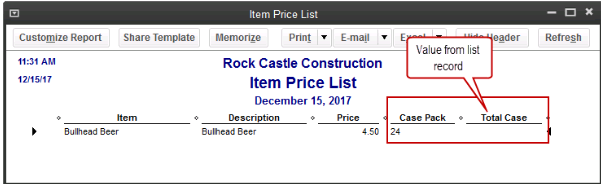

Sorting on Item Custom Fields

In prior versions, we had the ability to sort on the Customer and Vendor Custom Fields, but not on the Items Custom Fields – those fields were mostly notational and not very reportable.

In QuickBooks 2016 Premier, Accountant, and Enterprise, Intuit introduced this feature which will allow sorting on Inventory Valuation and Inventory Stock Status reports as well as the Inventory Price List. This will save countless hours of exporting to Excel and creating Pivot Tables to gather the required information.

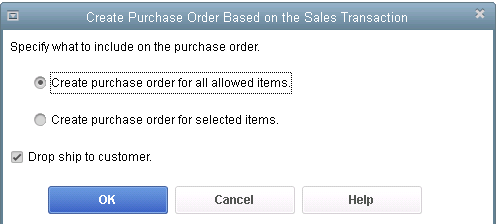

Auto Copy Ship to Addresses

For Contractors and Retailers who order materials or goods to be shipped directly to the job site or customer, QuickBooks 2016 – Premier, Accountant and Enterprise, has the ability to populate the Customer address in the Ship To Address directly from an Estimate or Sales Order, simply by selecting the Drop Ship to Customer checkbox when creating a Purchase Order.