As a business coach and advisor, one of the most impactful conversations I have with customers revolves around understanding what it takes to make a profit by analyzing their cost structure—specifically, distinguishing between fixed and variable expenses—and how that affects their breakeven point. Whether you’re running a construction company, a retail shop, or a bustling restaurant, mastering this concept can be the difference between survival and sustainable success.

Let’s break this down with clarity and real-world examples.

What Are Fixed and Variable Expenses?

- Fixed Expenses are costs that remain constant regardless of your business activity level. They do not change with sales or production volume.

- Variable Expenses fluctuate in direct proportion to your revenue or output. More sales revenue or projects means more variable costs.

Understanding the balance between the two helps you:

- Plan more accurately

- Price your services and/or products effectively

- Make better hiring and investment decisions

- Know exactly what it takes to break even—that is, to cover your expenses without incurring a loss.

Construction Industry

Variable Expenses:

- Job materials (e.g., concrete, lumber, flooring)

- Subcontractor fees (e.g., electricians, plumbers)

- Equipment rental (e.g., excavators, lifts, scaffolding)

- Direct labor on job sites (typically paid hourly)

- Direct labor burden (payroll taxes, workers compensation, benefits)

- Fuel and transportation related to specific projects

Fixed Expenses:

- Office rent or warehouse lease

- Business insurance premiums

- Salaried administrative staff

- Utility bills for a permanent office location

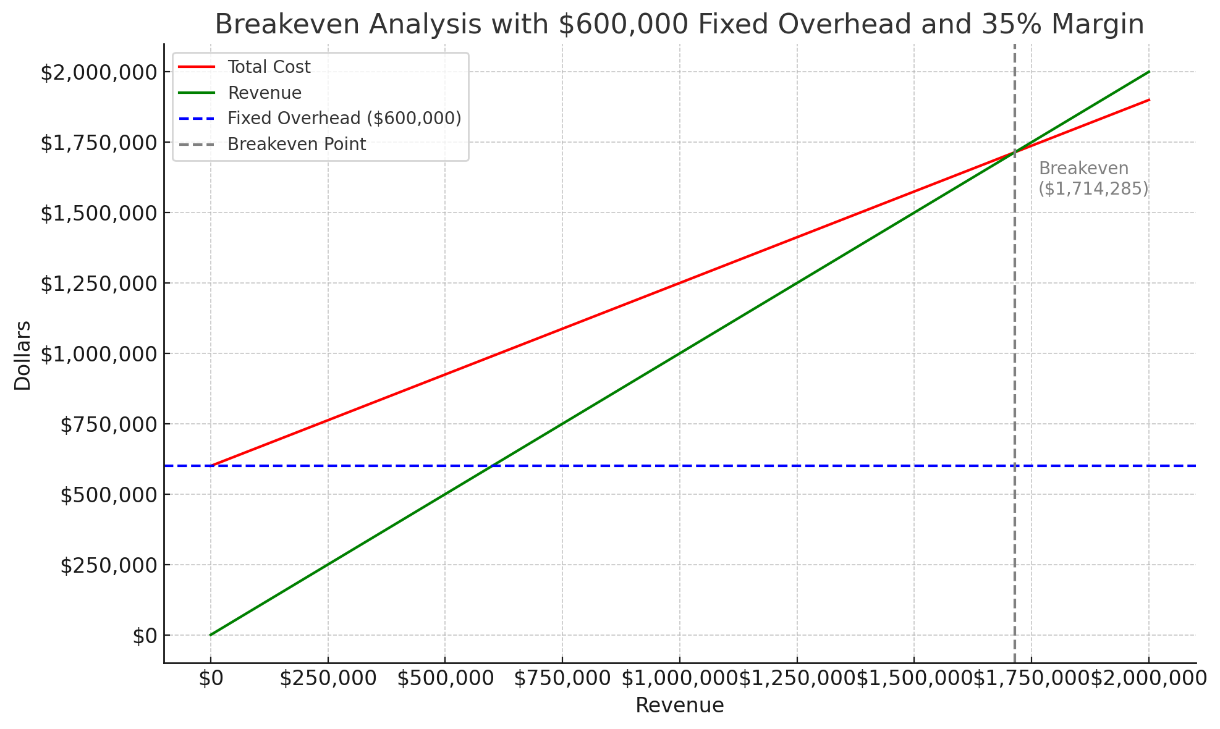

Breakeven Example: Let’s say your annual fixed costs are $600,000 and that you markup your variable costs to arrive at an average 35% contribution margin, that’s how much your projects contribute to covering the overhead.

Breakeven Revenue Formula

The breakeven point in terms of revenue is calculated as follows:

Breakeven Revenue = Fixed Costs / Contribution Margin

$600,000 / .35 = $1,714,285.71

You will need to generate $1,714,286 in revenue to break even and anything beyond that is profit.

Here’s the breakeven analysis in graph format:

- The blue dashed line shows your fixed overhead.

- The red line is your total cost (fixed + variable).

- The green line is your revenue.

- The gray dashed line marks the breakeven point, which is $1,714,286 in revenue.

This chart helps visualize exactly how much you need to bring in before turning a profit.

Why This Matters

When you clearly define your fixed and variable expenses, you’re better positioned to:

- Adjust pricing intelligently

- Manage payroll strategically during slow seasons

- Negotiate vendor contracts

- Scale your business with intention

Breakeven analysis isn’t just a math exercise—it’s a decision-making compass. When you know your breakeven point, you know exactly what you need to sell, build, or serve just to stay afloat—and how much more to hit your profit targets.

Final Thought

Every dollar you bring in above your breakeven point contributes directly to your profit—but only if you manage your variable costs wisely. Understanding this relationship helps you shift from reactive to strategic business operations.

If you’re unsure how to calculate your breakeven point or how your cost structure stacks up, let’s talk. We help construction, retail, and restaurant owners like you take control of their numbers so they can focus on growth with confidence.

Stay tuned for our next issue of Fun With Finance where we break this down for the retail and restaurant industries.

Effective inventory management is critical for small businesses in retail, food service, and manufacturing. Striking the right balance between having enough inventory and avoiding overstock can significantly impact your profitability and customer satisfaction.

Effective inventory management is critical for small businesses in retail, food service, and manufacturing. Striking the right balance between having enough inventory and avoiding overstock can significantly impact your profitability and customer satisfaction.

When inventory levels are too low, businesses risk running out of stock, leading to missed sales opportunities and unhappy customers. For manufacturers, insufficient raw materials can halt production, delaying order fulfillment and damaging your reputation. On the other hand, holding too much inventory ties up cash flow, leaving resources idle on shelves or in warehouses. Excess stock often leads to spoilage, especially in food service, where expiration dates and perishability are constant challenges. In retail, seasonal goods can quickly lose value, requiring deep discounts to clear outdated inventory.

Excess inventory is also susceptible to damage, theft, and increased insurance costs. Write-offs from unsellable goods directly impact your bottom line, while storage space may become a financial burden. Moreover, carrying surplus stock often means higher cash requirements, diverting funds that could otherwise support business growth or operational improvements.

To optimize inventory management, implement real-time tracking systems to monitor stock levels accurately. Establish clear re-order points to prevent shortages while minimizing overstock. Align your purchasing decisions with demand forecasts, ensuring you have the right products, at the right price, at the right time.

By prioritizing inventory management, your business can reduce waste, improve cash flow, and better meet customer needs—creating a solid foundation for long-term success.

As business advisors specializing in implementing accounting systems for small businesses and nonprofits, we can help you take control of your inventory with tools that provide real-time insights and automate critical processes. Contact us today to learn how the right system can streamline your operations, improve cash flow, and ensure your inventory works for you.

As we prepare to wrap up 2024, there’s no better way to set the stage for a successful new year than by finishing strong. A smooth year-end close not only gives you peace of mind but also sets you up to hit the ground running in 2025.

Here’s a comprehensive checklist to help you organize and streamline your year-end close. And remember, if any of these tasks seem daunting, we’re just an email away to assist!

Financial Tasks

- Catch up on your bookkeeping. If you’ve been putting this off, now’s the time to get your books in order to avoid the rush of tax season.

- Reconcile all bank accounts. Include savings accounts, PayPal, credit cards, and cash equivalents. Review old uncleared checks, void or re-issue, as necessary.

- Review and address unpaid invoices. Collect outstanding invoices from customers and clean up any errors in accounts receivable.

- Write off uncollectible invoices. Prepare your books for a realistic reflection of revenue.

- Record all bills due through year-end. Reconcile your accounts payable and ensure balances are accurate.

Payroll and Contractor Preparations

- Update employee and vendor addresses. Ensure accurate W-2s and 1099s by confirming everyone’s information is up to date.

- Gather W-9s from contractors. This simplifies your 1099 filing process.

- Request proof of workers’ compensation insurance. Avoid extra charges by collecting certificates from applicable contractors.

- Decide on year-end employee bonuses. Remember, these payments are subject to withholding taxes.

- Review PTO balances. Adjust or roll over unused days in your payroll system.

Inventory Management

- Schedule and take inventory. Make necessary adjustments to your books after counting.

- Write off unsellable inventory. If possible, sell scrap inventory or waste to recover costs.

Assets and Liabilities

- Update your fixed assets register. Confirm that you still own all of the assets listed on your depreciation schedule.

- Calculate and record depreciation as needed.

- Adjust loans for interest and principal allocations. (Need help accurately recording business loans? Check out this tutorial from our team.)

- Analyze all balance sheet accounts. Ensure all balances are current and accurate.

Tax Preparation and Strategy

- Plan your deductions. Decide whether to maximize deductions or defer income for optimal tax impact.

- Prepare for tax adjustments. Work with your accountant to ensure all entries and reconciliations are complete.

Recordkeeping and Organization

- Ensure a complete paper trail. Match transactions with receipts, invoices, and other documents.

- Digitize and store records. Scan and securely save important documents like bank statements, payroll reports, and contracts. (If you’re still operating your business using a local server to store your data, we wrote a think piece about why you should consider switching to cloud-based storage)

Strategic Planning for 2025

- Create a revenue and profit plan. Enter your 2025 goals into your accounting system. (Need help determining where your revenue should come from in 2025? Check out our article about three different sources of cashflow. Need to find out if your growth strategy actually optimizes your profits? Check out this tutorial we wrote.)

- Review holiday closures. Share your 2025 holiday schedule with your team.

- Update pricing. Adjust product and service prices if this is your annual review period.

- Review key metrics. Decide which performance indicators will guide your success in 2025.

Celebrate and Reflect

As you complete this checklist, take time to celebrate your accomplishments from 2024. Reflect on what went well and set your sights on an even better 2025. If you need help with any of these tasks, we’re here to make the process easier. Let’s close the year with confidence and start the new one with excitement!

We’ve heard numerous horror stories over the years of business owners falling victim to sophisticated phishing scams that compromise their operations, cost them thousands of dollars, and expose their customers to risk. Hackers are evolving rapidly, making it harder to distinguish between malicious threats and everyday emails.

Our goal here is to empower, not scare you. The good news? Many of these threats are avoidable with vigilance. Hackers are even craftier than before, and phishing schemes have adapted to exploit newer technologies. However, with a few best practices, you and your team can keep your data safe from current phishing trends.

Below, we outline some common phishing threats and offer ways to safeguard against them.

Common Threat 1: Impersonation of Accounting or Financial Software

Phishers continue to target users of popular accounting software, impersonating platforms like QuickBooks with claims such as “Your file is corrupted,” “Your payment method is expiring,” or “Your software needs an urgent upgrade.” The goal is to either convince you to pay for a fake service or grant them access to your system.

How to dodge the threat: Always verify the sender’s email address. Emails from Intuit or QuickBooksⓇ will end with “@intuit.com” or “@quickbooks.com.” If you receive a suspicious email, permanently delete it. Do not provide sensitive information or remote access to anyone unless they are a trusted, verified partner.

Common Threat 2: The Rise of AI-Assisted Phishing

Hackers are now leveraging AI tools to generate phishing emails that mimic legitimate communications. These emails may come from familiar addresses or look nearly identical to a colleague’s typical correspondence, including personalized details that make the email seem even more credible.

How to dodge the threat: Never click on links or download attachments from unexpected emails, even if they appear to come from trusted contacts. Always hover over links to preview the URL and verify its legitimacy. AI tools are being used both by hackers and cybersecurity experts, so staying ahead of phishing trends is more important than ever.

Common Threat 3: “You Have Voicemail,” “Urgent Invoice,” and “Thanks for Your Purchase” Emails

While voicemail and invoice phishing schemes aren’t new, hackers are increasingly using these tactics to create a sense of urgency. You might receive an unexpected email about a voicemail or invoice, often from a service you don’t use. In addition, we’ve seen emails alerting you to free prizes – you’ve won a free trip – with a link to click to claim your prize.

Lastly in this category, there is a new strategy in which phishers send “confirmation” emails suggesting that you’ve made a subscription purchase, going so far as to even include a pdf of a phony receipt.

How to dodge the threat: If something feels off, it probably is. Never download an attachment or follow a link without verifying the source through another channel. Call the service provider directly to check whether they sent the email, and always be wary of “business” emails that end in @gmail.com, @yahoo.com, etc.

Common Threat 4: The QR Code Swap

QR codes have become a ubiquitous tool, especially in restaurants and retail. However, phishers now use QR codes to disguise malicious URLs. They may overlay fake QR codes in public spaces or send phishing emails with QR codes that link to compromised websites or malware.

How to dodge the threat: Before scanning a QR code, double-check its placement and ensure it hasn’t been tampered with. After scanning, review the web address that appears and make sure it’s legitimate before clicking. If something feels suspicious, don’t scan the code.

Common Threat 5: Social Engineering on Social Media

Phishing attacks are increasingly moving to social platforms like LinkedIn and Facebook. Hackers may pose as recruiters, customers, or industry professionals to extract personal information or trick you into downloading malicious files.

How to dodge the threat: Be wary of unsolicited messages from strangers on social media, especially those requesting personal details or sharing links. Always verify the identity of anyone asking for sensitive information and avoid clicking on unknown links shared via direct messages.

Best Practices: Staying Secure in the Age of Evolving Phishing Tactics

While phishing techniques continue to evolve, the core defenses remain the same: vigilance, awareness, and caution. Here are some key best practices to follow:

- Set up multi-factor authentication (MFA): Use MFA wherever possible. This could involve receiving a code via text, email, or through an authenticator app like Google Authenticator. MFA adds an extra barrier for hackers, making it far less likely they’ll succeed even if they gain access to your credentials.

Use strong, unique passwords: Password management apps like LastPass or 1Password can generate complex passwords and securely store them. Avoid reusing passwords across different accounts. - Stay informed on new phishing tactics: Cybercriminals are constantly adapting. Subscribe to trusted cybersecurity news outlets like PCMag, Forbes, or TechCrunch to stay updated on the latest phishing techniques.

- Train your team: Cybersecurity isn’t just an IT responsibility—it’s an organization-wide effort. Conduct regular phishing simulations and training sessions to ensure that your employees recognize suspicious activity and respond appropriately.

- Don’t open doors for strangers: Whether in person or online, never allow someone to access your computer or accounts unless you have verified their identity through an established and trusted channel. If in doubt, don’t engage.

- Verify email senders: Always check email addresses carefully. A small typo or strange domain could indicate a phishing attempt. Cross-check with trusted sources if something feels off.

- Use secure file-sharing methods: When sending or receiving sensitive information, avoid doing so via email. Use encrypted file-sharing services like SmartVault or similar tools.

- Trust your instincts: If something feels off, don’t proceed. Whether it’s a weirdly worded email or a strange request, your gut is often a good first line of defense against phishing attempts.

It’s more important than ever to remain cautious and aware of evolving cybersecurity threats. Phishing is becoming more sophisticated, but by staying alert and following these best practices, you can protect your business and personal data from harm.

If you’re unsure about an email or solicitation, especially related to your accounting software, reach out to us. We’re always here to help!

As a business coach, I’ve often witnessed the power of familial bonds in the world of entrepreneurship. One strategy that has shown immense potential for both the business and the family is hiring children within the business. While some may raise eyebrows at the idea, there are numerous benefits to be reaped from such a decision, ranging from financial advantages to fostering a sense of responsibility and entrepreneurship in the younger generation.

As a business coach, I’ve often witnessed the power of familial bonds in the world of entrepreneurship. One strategy that has shown immense potential for both the business and the family is hiring children within the business. While some may raise eyebrows at the idea, there are numerous benefits to be reaped from such a decision, ranging from financial advantages to fostering a sense of responsibility and entrepreneurship in the younger generation.

Two Financial Benefits of Hiring Your Children in Your Business

Hiring your children and offering them a salary can be a mutually beneficial scenario, financially speaking:

- Salary Expenses: Instead of handing out allowances, you can pay them a reasonable wage for the work they do. The IRS allows business owners to deduct reasonable wages paid to their children as a business expense.

- Tax Advantages: Hiring your children can also offer tax advantages for both parties. Children can earn up to a certain amount (subject to change, so consulting a tax professional is advisable) without paying federal income tax. For the business, wages paid to children are deductible as a business expense, reducing the overall taxable income.

Tax Exemptions and Retirement Benefits Associated with Hiring Your Children

As a business owner, it’s also important to understand the potential tax benefits of providing certain benefits to your employees, including family members. In particular, offering retirement planning as a benefit to your children can both introduce them to the concept of saving early on and yield tax advantages for your family. Let’s get into the details:

Tax Exemptions for Certain Benefits: Depending on the structure of your business and the tax laws in your jurisdiction, certain benefits provided to employees, including your children, may be tax-exempt. This could include health insurance premiums or contributions to retirement plans.

Retirement Planning as a Benefit: By hiring your children, you can also introduce them to the concept of retirement savings early on. You may establish retirement accounts, such as a Roth IRA, and contribute a portion of their earnings. This not only helps them start saving for their future but also reduces the family’s overall tax liability.

Three Final Benefits of Hiring Your Children within Your Small Business

Hiring your children can reap benefits beyond providing you and them financial and tax-savings benefits. This decision can also offer them a meaningful learning opportunity and set the stage for their future success, both professionally and financially. Here are three final benefits of hiring your children within your small business:

- Hiring your children provides them with a learning opportunity: Working in the family business provides invaluable real-world experience for children. They learn important skills such as communication, teamwork, problem-solving, and financial literacy, all of which are crucial for their future endeavors.

- Hiring your children creates an opportunity for family bonding: Working together can strengthen family bonds and create shared experiences. It provides an opportunity for open communication and mutual understanding between generations, fostering a sense of unity and purpose within the family.

- Hiring your children allows for proactive succession planning: Hiring children can be a strategic move for succession planning. It allows them to gain firsthand experience and knowledge of the business, preparing them to take on leadership roles in the future.

Ultimately, hiring your children in your business can be a win-win situation for both the family and the business. This business strategy offers financial benefits, tax advantages, and valuable learning opportunities while fostering a strong sense of family unity and preparing the next generation for future success.

However, it’s essential to approach this decision thoughtfully and in compliance with all legal and tax regulations. Consulting with a qualified tax advisor or financial planner is a great way to navigate the complexities–and maximize the benefits–of this arrangement.

As a business coach, one of the fundamental lessons I impart to my customers is the vital importance of cash flow management. Cash flow is the lifeblood of any business, and understanding the primary avenues through which cash is generated can make the difference between thriving and merely surviving. There are essentially three ways to generate cash for your business: through operations, financing, and investing. Let’s delve into each of these in more detail.

1. Cash from Operations: Doing What You Do Best

Generating cash from operations is the most sustainable and preferable method for a business. It involves the day-to-day activities that your business engages in to generate revenue. Your operations cash flow is like the engine room of your enterprise, where the core products or services are created, marketed, and sold.

The key business priorities for generating cash from your operations include the following:

- Generating revenue: This includes sales of goods or services. Consistently increasing sales while managing expenses effectively is crucial.

- Managing expenses: Controlling operating expenses ensures that more of your revenue is converted into profit.

- Improving efficiency: Streamlining operations can reduce costs and improve productivity, in turn boosting cash flow.

Prioritizing operational cash flow is vital to a successful business because it indicates a healthy, self-sustaining enterprise. Managing the above priorities while enhancing customer experience, optimizing pricing strategies, and continuously improving product or service quality will drive your operational cash flow.

2. Cash from Financing: Leveraging Debt and Equity

The second avenue of generating cash flow is financing, which involves borrowing money or raising funds from investors. While less ideal than generating cash from operations, financing is sometimes necessary to support growth, manage working capital, or navigate challenging times.

There are two primary types of financing:

- Debt Financing: This includes taking out loans or issuing bonds. While debt must be repaid with interest, it can provide immediate funds for expansion at a critical time for growth (or other needs).

- Equity Financing: Selling shares of your company to investors in exchange for capital. This doesn’t require repayment but does dilute ownership.

Financing can be a double-edged sword; it can provide the necessary capital to seize growth opportunities, but it also comes with risks, such as interest obligations and potential loss of control. A sound financing strategy should balance these risks, ensuring that debt levels remain manageable and that equity is only diluted when it aligns with long-term goals.

2. Cash from Investments: Selling Assets

The third method is generating cash by liquidating investments you’ve made for your business. This strategy can include selling off assets, such as equipment, real estate, or even entire business units that are no longer core to your business strategy.

Below are three critical considerations for your investing activities:

- Asset Management: Regularly review your asset portfolio to identify non-essential or underperforming assets.

- Strategic Sales: Consider selling non-core assets to free up capital, which can be reinvested in higher-return areas of your business.

- Investment Income: Earning returns from financial investments can also contribute to cash flow.

This method can provide a significant influx of cash but should be approached cautiously. It’s essential to ensure that selling assets aligns with your long-term strategic goals and doesn’t undermine your operational capabilities.

Balancing your Cash Flow Sources

Each of these three sources of revenue has its place in a comprehensive cash flow strategy. Remember, cash from operations is most reliable, and wisely leveraging financing can support growth and stability. At the same time, strategic asset sales can optimize resource allocation. All three avenues can help your business grow and remain stable. Strategically integrating these three methods of generating cash could look like this:

- Optimizing your operations to boost cash flow by improving efficiency and controlling costs.

- Seeking financing to invest in new technology to expand your capacity to produce

- Selling outdated equipment to raise additional funds.

As your business coach, my goal is to help you navigate these avenues effectively, ensuring your business can not only survive but thrive in any economic climate. As always, if you have any questions or want to learn more about cash flow management services for your business, please feel free to contact us anytime.

Implementing a new accounting system is no small feat. It requires careful planning, coordination, and commitment from every team member. We’re always excited to help a business with a new accounting infrastructure implementation because we know the positive impact it can have on a business.

We also understand that, as a business owner, transitioning to a new software solution can be both exciting and daunting. You’re taking a giant leap in a positive direction to increase your efficiency, enhance the functionality of your accounting system, and optimize your processes.

But great reward doesn’t come without some risk: you’ve likely already considered employee learning curves, potential technical challenges during the transition period, and how a new implementation could disrupt daily operations. These concerns are valid, and with the right expectations, the journey can be smoother and more rewarding for everyone involved.

Hard Work Ahead: Embracing the Challenge

Let’s be honest: implementing a new accounting system isn’t a walk in the park. It requires time, effort, and resources to ensure a successful transition. From data migration to process reengineering, numerous tasks need to be completed with precision and attention to detail. It’s a journey that will test the resilience and determination of the entire team.

Rowing in the Same Direction: Unity in Purpose

Implementing a new accounting system requires a collective effort from your entire team. Everyone on board must be rowing in the same direction; if you notice team members resisting the change, it’s best to address the issue head-on. Ultimately, the goal is not to make their jobs harder; it’s to improve their workflows and processes in the future by putting in the hard work now. And for your implementation to be as successful and pain-free as possible, every team member must be ready to embrace change, adapt to new processes, and support one another throughout the transition. With a company culture of collaboration and communication, we can overcome any challenges that come our way while implementing your new accounting infrastructure.

Charting the Course: Milestones and Deadlines

Like any major project, implementing a new accounting system involves setting milestones and deadlines to keep the team on track. These milestones serve as checkpoints to assess progress and make necessary adjustments along the way. Whether we’re completing data migration or conducting one-on-one training with your team, each milestone brings us one step closer to our ultimate goal: to give you a beautiful accounting infrastructure that meets your current business needs and still leaves room for growth.

Bringing It All Together: The “Go Live” Date

The “go live” date is the culmination of your months of hard work and preparation. It’s the moment when the new accounting system officially replaces the old one, and all systems are a go! Reaching this milestone involves coordinating a multitude of moving parts, from finalizing configurations to conducting system testing. Everyone needs to be aligned and working together towards this common goal.

Embracing Differences

Transitioning to a new accounting system inevitably brings about comparisons between the old and the new. From software functionalities to workflow processes, there will be changes that require adjustment and adaptation. It’s important to acknowledge these differences and approach them with an open mind and a willingness to learn. We wouldn’t be guiding you through an implementation if we didn’t already understand your business’s unique needs and believe we were charting the best path forward for you. With the right mindset, we can turn the differences between your former and future accounting systems into opportunities for growth and improvement.

Implementing a new accounting system is a significant undertaking that requires dedication, perseverance, and teamwork. By setting clear expectations and rallying the team around a common goal, we can confidently navigate this journey and achieve success. You can learn more about our implementation services here.

Time is a precious, valuable, and finite resource. We all have only twenty-four hours in a day and only seven days in a week to get everything done. And for entrepreneurs, that can often seem like barely enough.

So, why does it seem like some of us can get more done in a day than others? The answer could lie in a few possibilities:

- Are you doing what’s important or simply what seems to be the most urgent at the moment?

- Are you wasting time on tasks that should be delegated, automated, or ignored completely?

- Have you ever considered tracking what you spend your time on?

I was curious about how I really used my time, so I tracked my time and activities for one week. I uncovered valuable information regarding inefficiencies in my world and have been able to take steps to eliminate, automate, and delegate better. I encourage you to do the same, and this article should help you get a good start on reclaiming your time and working more productively.

Day 1: Establish the Habit of Time Tracking

- Begin your day by setting up a simple time-tracking system. Whether you prefer digital tools or the classic pen and paper, make a note of every task and its duration.

- Be honest about where you’re spending your time. This is a judgment-free zone, and having more accurate information here will only benefit you in the long run.

- Reflect on what’s driving your activities:

-

- Are you stuck in an endless loop of emails?

- Are you using your inbox as a to-do list?

- Are you wasting time on technology issues?

- Are you answering the same questions over and over from team members or customers?

Day 2-6: Document Your Activity, Reflect on Your Data, and Adjust Your Habits Accordingly

- Log your activities throughout each day, including breaks and interruptions.

- At the end of each day, reflect on the activities you tracked. What surprises you? What patterns emerge?

- Identify tasks that took longer than expected or seemed unproductive.

Day 7: Analyze Your Data and Strategize Improvements

- Compile your week’s data. Look for trends, time wasters, and areas (or times of day) where you were most productive.

- Categorize these activities into groups:

-

- Critical tasks – those that only you can do

- Enjoyable tasks – Those that you really like to do

- Delegate-able tasks – Things that you could outsource or delegate to your team

- Automatable tasks – recurring activities that could be completed more efficiently with technology

- Useless tasks – activities with minimal impact that could be eliminated; you’re only doing them because you’ve always done them, and practice makes permanent

Next steps: Delegate and Automate

- Pinpoint tasks that could be delegated to your capable team members, or outsourced to a vendor. Empower your team members, entrust them with responsibilities, and create standard operating procedures on how these tasks should be done to your specifications. Even if it feels like training your team will only make the process take longer, in the long-term, delegating tasks to your team will free up your time for strategic decision-making activities.

- Research opportunities to automate repetitive tasks and leverage technology to save time and reduce errors.

- Be open to the possibility that certain tasks may not be adding significant value and consider eliminating or outsourcing them to focus on what activities will have the greatest impact on your business.

Starting 2024 off on the right foot

This exercise may seem simple but its impact can be profound. Its purpose goes beyond increasing efficiency – it’s about creating a business that thrives on your unique strengths.

By gaining insight into how you allocate your time, you’ll be able to identify areas for improvement, empower your team to take on more responsibility, and free up valuable time for more rewarding and impactful activities.

Time is your most valuable asset, and by mastering the art of effective time management, you can unlock doors to unparalleled productivity and success. I look forward to hearing about your time-tracking experience and findings in our next coaching session.

Regards,

Rhonda Rosand, CPA

CEO, New Business Directions

Cloud Hosting: It’s Time to Break Up with Your In-House Servers.

Gone are the days of dial-up internet and cell phones with buttons for every letter of the alphabet. Neither dial-up nor the Blackberry makes sense in 2023, and frankly, neither does the in-house server. The current era of business demands that your data and software be readily accessible; cloud hosting is the best way to accomplish this.

Cloud hosting is the process of storing your software and data somewhere other than the box under your desk that’s collecting dust.

It requires no more installs, re-installs, updates, or worries about backups. It allows you to work from anywhere, at any time, collaborate effortlessly with your team and professional service providers, and scale your operations –without the IT headaches.

The cloud is safe and secure with built-in redundancies, managed IT (think firewalls and virus protection), and is part of a comprehensive disaster management plan, allowing you to eliminate the responsibility of managing it yourself while increasing the accessibility of your software and data.

Anything can happen in business — your server can crash, your office can flood, your back-up could be corrupted. Your financial data is the lifeblood of your business, and safeguarding it with modern technology like cloud hosting is essential.

I’ll never forget my first tax season at a local CPA firm, one customer meeting in particular. We were sitting across the table from a nice young couple expecting their first child. They had started a small construction company that year and did quite well. The purpose of our meeting was to deliver the tax return, tell them the balance due for taxes, and answer any questions they might have about the Federal and state tax returns and future estimated tax payments.

When I shared with them that they owed just shy of $10,000 in income taxes, the young lady burst out in tears! They didn’t have the money. They had profits–but no cash. No one had ever explained the difference to them, and they were not expecting a balance due of that magnitude.

This meeting changed their lives and the course of my career. I never again wanted to sit across the table to deliver unexpected news to a bright-eyed entrepreneur and his expecting wife.

Therein began my career of teaching small business owners the difference between profits and cash, along with many other nuances of business ownership that no one ever tells you (including the fact that approximately 40% of your profits will go to pay income taxes). It’s a harsh reality, and knowledge is power. These outflows of cash can be planned when you have advanced notice. This type of planning is usually called tax planning, business planning, revenue planning, and/or profit planning. But knowing the difference between profit and cash is a good place to start — let’s dive in.

Here is the short and sweet on the difference between profits and cash. Profit is revenue minus expenses. Cash is money in minus money out. There is a fancy, seldom understood financial report called a Statement of Cash Flows that reconciles your profit to your cash, and is part of a comprehensive financial statement package which will also include your Balance Sheet and Profit and Loss Statements.

Most small business owners only look at the profit and loss, pay little (if any) attention to the balance sheet, and have never heard of the Statement of Cash Flows.

However, I would argue that the Statement of Cash Flows is the single most important financial report. It will tell you how much profit you made, where the money went, and what’s left of your profit.

There are certain things that you spend money on that are not tax deductible: some are not deductible at all, and some not immediately. They use cash, deplete your bank account, and do not reduce profits.

Let’s discuss a few common examples:

Equipment – you buy a new piece of equipment for your business. This might look like a walk-in cooler for a restaurant, a forklift for a warehouse, a work van for a construction company, a new stitcher for a manufacturing facility, or a company truck for the business owner. These items are Assets with a useful life extending beyond a one-year operating cycle and are reported on the balance sheet. They affect cash and do not affect profit until they are depreciated. When you make an investment in a piece of equipment like this, it is not immediately deductible. You’re out the cash and do not have an expense deduction–yet.

Loan Payments – Let’s say you buy that forklift and take a loan for it because the interest rate is better than what you’re making on your savings, or you don’t actually have the cash to pay for it outright. While the interest paid on the loan will be tax deductible, the loan payments themselves are not. The principal portion of the loan payment reduces the loan Liability account on the balance sheet. It affects cash, but never profits.

It is important to reconcile profits to cash, to find out where the money came from and where the money went. You never want to be caught short at the end of the year without enough cash to pay the taxes on the profits generated by your business. And hey, those federal income taxes you pay? Those are not tax deductible either.

While New Business Directions doesn’t prepare tax returns, our clients can benefit from the types of planning we mentioned above. Having a CPA in your corner throughout the year can make or break you at tax time–we can consult with you on the best time to make a capital expenditure decision, keep you informed about the speed at which cash is entering and leaving your business, and more. If you’d like to discuss cash vs. profit within your company, complete our intake form to get started.