It’s good to know some basic accounting terms, and here are ten terms with friendly definitions for your review.

Asset: Essentially, assets are what you own. These include your bank accounts, business equipment, and even the amounts that customers owe you.

Revenue: Revenue is what you make. Another word for it is Sales. You generate revenue in your business when you make a sale to a customer. The amount of the sale is included in revenue.

Expense: An expense is what you spend in your business on items that are not expected to benefit you in the long term. Expenses include credit card fees, office supplies, insurance, rent, payroll expense, and similar items that you need to incur to keep your business running.

COGS: COGS stands for Cost of Goods Sold. It’s a form of expense that directly relates to the product or service being sold. For example, if shoes are being sold, the cost of purchasing those shoes are consider COGS, while something like rent or insurance is simply an expense. COGS is more important in manufacturing, retail, and distribution companies.

Net Income: Another word for net income is profit. It’s calculated by subtracting expenses from revenue. If what’s left over is a positive number, it’s net income and if it’s negative, it’s a net loss. Besides your salary, it’s the amount of money you can either keep or re-invest into your business.

Debit: A debit is a term that tells you whether money is being increased or decreased. The hard part is that it’s opposite depending on the account and the company. Here are some examples:

- A debit to cash increases it, so that’s good.

- A debit to a loan you owe decreases it, so that’s good too because you are paying it off.

- When you talk to a bank teller and they want to debit your account, it means they are taking money away, because your account is a liability to them. So it’s opposite.

Credit: A credit is a term that tells you whether money is being increased or decreased. The hard part is that it’s opposite depending on the account and the company. Here are some examples:

- A credit to cash decreases it, as in writing a check to someone.

- A credit to a loan you owe increases it, so you owe more money.

- When you talk to a bank teller and they want to credit your account, it means they are putting money in, because your account is a liability to them. So it’s opposite.

GAAP: GAAP stands for Generally Accepted Accounting Principles. It refers to the set of standards that must be followed by accountants when creating accounting reports for people like bankers and investors who rely on them.

Liabilities: Liabilities are what you owe. If you have loans taken out for your business or owe vendors money for invoices of purchases they sent you, those are liabilities. Common liabilities include sales tax that you’ve collected but not paid, unpaid vendors’ invoices, credit cards that are not paid off each month, mortgages on buildings, and any bank loans you’ve taken out.

Equity: In mathematical terms, equity is the net of your assets less your liabilities. In more philosophical terms, it’s the net amount you and your fellow business owners have invested in your business adjusted by the years of net income you’ve made less what you’ve taken out of the business.

How many terms did you already know? Do you feel smarter already? Knowing accounting terms will help you understand this aspect of your business a bit better.

QuickBooks 2016 Desktop was recently released and there are a few new features that you will want to take a look at to see if it has something worth upgrading for.

Bill Tracker

The Bill Tracker is similar to the Income Tracker in the Customer Center that was released as a new feature in QuickBooks 2014 and improved with QuickBooks 2015. The Bill Tracker is located in the Vendor Center and allows a Snapshot View of Purchase Orders, Open Bills, Overdue Bills and Bills that have been paid in the last 30 days. Transactions can be managed from this area and batch actions can be taken to print or email and to close Purchase Orders and Pay Bills.

This Fiscal Year-to-Last Month

In the past, we had choices for date ranges on financial reports of This Fiscal Year or This Fiscal Year-to-Date as well as This Month or This Month-to-Date, none of which worked well for month-end reporting purposes. We now have This Fiscal Year-to-Last Month which allows us to print our financial reports as of the end of the Last Month, through which accounts are typically reconciled. This will allow us to Memorize Reports with the correct date instead of saving with a Custom Date that needs to be changed each time.

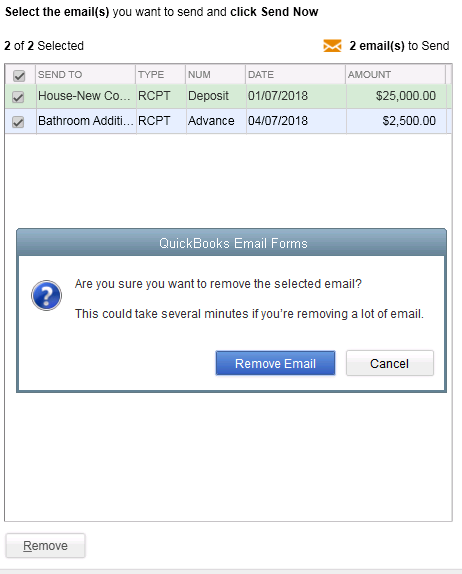

Bulk Clear “Send” Forms

Bulk Clear “Send” FormsSales Receipts, Invoices, Estimates and Purchase Orders all have an Email Later check box and it’s a “sticky” feature, meaning that once selected, it remembers for future transactions. In the past, we would accumulate many documents in the queue to be sent later and if we wished to clear the queue, it would have to be done individually. With this release, under the File menu, Send Forms, we can now Select All and click Remove.

do a Backup!

We are pleased to announce that on November 18th, 2015, Rhonda Rosand, CPA/Owner of New Business Directions, will be conducting the QuickBooks 2016 Expanded workshop sponsored by the New Hampshire Society of Accountants at the Executive Court in Manchester, NH.

Rhonda will touch on What’s New in QuickBooks 2016, how to fully utilize QuickBooks, which software program works best for you and your clients, and an accountants only section leaving plenty of time for questions.

Registration fee is $89 for NHSA members and $109 for non-members and allows participants to earn 4 CPE credits. To sign up for this event, please call (603)228-1231 or email info@cornerstoneam.com

On November 2nd– 4th, Intuit will be hosting the 2nd annual QuickBooks Connect Conference in San Jose. The conference brings together thousands of entrepreneurs, small business owners, accounting professionals and developers  under one roof.

under one roof.

There are three different tracks on the agenda as follows:

Accountant – QuickBooks Connect will help your firm get future ready by challenging you to go further, think differently, and embrace the cloud to properly value the services you provide, grow your firm, and better support your clients. *

Small Business – Whether you’re a company of one or one hundred, come to make your business dream a reality: network with fellow small business owners, entrepreneurs, self employed individuals, startup founders, and Venture Capital leaders to receive personalized advice on maximizing your success. *

Developer – Engage Intuit Developer experts to speed your QuickBooks app integration and successful launch to the QuickBooks ecosystem. Take advantage of the unique opportunity to meet and network with other developers, accountants and small business owners. *

The mission is to connect, learn and grow throughout a dynamic agenda of main stage and intimate sessions. Key speakers  include Oprah Winfrey, Jessica Alba, Brian Lee and Robert Herjavec. Sessions topics include: Here to There: The Accountant’s Journey toward Professional Greatness, Work/Life Harmony, 10 Barriers to Service Excellence and How to Overcome Them, and Cash is King: Tips to Increase Your Cash Flow Today. There will also be speed mentoring sessions and an entire series of QuickBooks Online training topics.

include Oprah Winfrey, Jessica Alba, Brian Lee and Robert Herjavec. Sessions topics include: Here to There: The Accountant’s Journey toward Professional Greatness, Work/Life Harmony, 10 Barriers to Service Excellence and How to Overcome Them, and Cash is King: Tips to Increase Your Cash Flow Today. There will also be speed mentoring sessions and an entire series of QuickBooks Online training topics.

Rhonda Rosand states, “This will be my second year attending the Intuit conference and I look forward to seeing many familiar faces at the event and I invite you to join me in California for this spectacular training opportunity.”

* – content is taken directly from the QuickBooks Connect Website

Small business owners have a lot on their plates, and time simply does not allow you to become an expert in all the areas required for running a business. Here are a couple of common mistakes that we see all the time. Correcting them will help you be more productive and profitable in your business.

1. Mismanaging receipts

Maintaining receipts are challenging for everyone, but the IRS requires that you have proof of business expenditures. Periodically, we come across people who feel that keeping the credit card statements are enough; unfortunately, they’re not. You’ll want to create a process to keep your receipts all in one place so they don’t get lost.

Receipts printed on thermal paper (think gas station receipts and many more) will fade within a year or two, and the bad news is the IRS could audit several years back if they come calling. Correct this by scanning them in or taking a clear picture of them using your smartphone.

Some accounting systems and/or document management applications allow you to upload the receipt and attach it to the transaction in your accounting system. This is a great solution, and if you’re interested in this, please ask us about it.

2. Ignoring the accounting reports

There are gold nuggets in your accounting reports, but some business owners don’t take the time to review them or are uncertain about how to interpret them. Your accountant can help you understand the reports and find the gold nuggets that can help you take action toward profitability.

Some of the things you can do with your reports include:

- Identifying your highest selling services or products

- Projecting cash flow so you’re not caught short at payroll time

- Getting clear on your top customers or your demographic of top customers

- Evaluating your marketing or business development spend

- Pointing out trends compared to prior years, budget, or seasonality effects

- Checking up on profit margins per product or service to make sure you are priced correctly

- Managing aging receivables or speeding up collections

- Measuring employee profitability, if relevant

- And so much more

Being proactive with your accounting will help you spot opportunities in your business that you can act on, as well as spot and correct problems long before they manifest into trouble.

3. Mixing business and pleasure

In your bank accounts and on your credit cards, mixing business and pleasure is to be avoided when possible. All businesses should have a separate bank account, and all business transactions should go through there. It takes an accountant much longer to correctly book a business deposit that was deposited into a personal account.

Taking out a separate credit card and putting all your business transactions on it will save your bookkeeper a ton of time. The credit card doesn’t even have to be a business credit card. It can just be a personal credit card that’s solely used for business. If you have employees making credit card charges, sometimes a separate card for them helps you control fraud.

The hardest area in which to separate business from pleasure is cash transactions. Be sure your accountant knows about these. The accountant can either set up a petty cash account or a reimbursement process so that you can get credit for cash expenditures that are for the business.

How did you rate on these three mistakes? Avoid these three and your accounting department as well as your business will run a lot smoother.

As a business owner, you’re likely torn in a hundred different directions every day. It can take up most of the work day just fighting fires, serving your customers, and answering employee questions – never mind the time spent on email. It’s super-easy to lose sight of what you can be doing to move your business forward the most.

That’s when “the one question” can come in handy. It’s something you can ask yourself at the very beginning of each day, even before you check your email. Make your question about you and your goals for your company.

That’s when “the one question” can come in handy. It’s something you can ask yourself at the very beginning of each day, even before you check your email. Make your question about you and your goals for your company.

The one question is, “What’s the highest payback thing I can do today?”

If your goal is to boost profits, then ask “What’s the highest payback thing I can do today that will boost my profits?” If your goal is to empower your employees, then ask “What’s the highest payback thing I can do today that will empower my employees?” If your goal is to make a difference in your community, then ask “What’s the highest payback thing I can do today to make a difference in my community?” If your goal is something else, tailor your one question to that specific goal.

It’s not about fighting fires or answering routine employee questions or even serving current  customers. Although those tasks are all important and essential, none of them will take your business to the next level.

customers. Although those tasks are all important and essential, none of them will take your business to the next level.

It could be meeting with a power partner or referral source that sends you a lot of business, designing the next campaign that will bring in a higher level customer, meeting with your employees for lunch, or researching new products to sell. It’s going to be a task that gets you working “on” your business instead of “in” your business.

If you like this idea, consider writing the question on a sticky note and posting it to your bulletin board so that you can see it  every day. I write my question and my intentions each morning on a colorful piece of paper that I carry with me all day. I do this while having my coffee and long before I check an email, text or telephone message.

every day. I write my question and my intentions each morning on a colorful piece of paper that I carry with me all day. I do this while having my coffee and long before I check an email, text or telephone message.

Try asking yourself this one question each day: “What’s the highest payback thing I can do today?” Then do it, and watch your business grow.

As we move into the fall season and the final quarter of the year, it’s a perfect time to commit to a project in your business that will help you reach the year’s end in better shape. Here are five ideas:

1. Back-to-School Time

If payroll expenses are one of the higher costs in your business, then it makes sense to boost your team’s productivity and maybe also your own. Fall is back-to-school time anyway, so it’s a natural time of the year to take on a course, read a business book, or hire an organizer to help you get more from your workspace.

If you spend a lot of time doing email, consider taking a course on Microsoft Outlook® or even Windows; learning a few new keystrokes could save you tons of time. If you need more time, look for a book or course on time management. Look for classes at your local community college or adult education center.

2. A Garage Sale for Your Business

Do you have inventory in your business? If so, take a look at which items are slower-moving and clear them out in a big sale. We can help you figure out what’s moving slowly, and you might even save on taxes too.

3. Celebrate Your Results

Take a checkpoint to see how your revenue and income are running compared to last year at this time. Is it time for a celebration, or is it time to hunker down and bring in some more sales before winter? With one more quarter to go, you have time to make any strategy corrections you need to at this time. Let us know if we can pull a report that shows your year-on-year financial comparison.

4. Get Ready for Year’s End

Avoid the time pressure of year’s end by getting ready early. Review your balance sheet to make sure your account balances are correct for all transactions entered to date. You will be ahead of the game by getting the bulk of the year reviewed and out of the way early.

Also make sure you have the required documentation you need from vendors and customers. One example is contract labor that you will need to issue a 1099 for; make sure you have a W-9 on file for them. If we can help you get ready for year-end, let us know.

5. Margin Mastery

If your business has multiple products and services, there may be some that are far more profitable than others. Breaking these numbers out to calculate your profit margins or contribution margins by product or service line can help you see the areas that are adding the most income to your bottom line. Correspondingly, you can determine if you have any items that are losing money; knowing will help you take the right action in your business. Refresh your financials this fall with your favorite idea of these five, or come up with your own fall project to rejuvenate your business.

contribution margins by product or service line can help you see the areas that are adding the most income to your bottom line. Correspondingly, you can determine if you have any items that are losing money; knowing will help you take the right action in your business. Refresh your financials this fall with your favorite idea of these five, or come up with your own fall project to rejuvenate your business.

Some numbers need reviewing on a daily basis, and one example of this is cash. When cash is coming in from a number of places, it’s great to have a daily summary of what was collected.

It’s also great to make sure all the collections hit your bank account so you can feel confident that no errors were made along the way. A daily cash reconciliation report will serve both needs very well.

A daily cash report will vary depending on the type of business you have, but it will look like a combination of a bank reconciliation and a sales report wrapped into one.

If you are managing your cash closely from day to day, then this report will help you stay sane. You’ll need two very brief spreadsheets to get started. The first one below is your daily sales from all sources. Your accounting system may be able to generate this.

| Today’s Sales | |

| Cash | $300.00 |

| Checks | $600.00 |

| Total Bank Deposit | $900.00 |

| Mastercard Visa | $400.00 |

| American Express | $200.00 |

| Total Credit Card Due | $600.00 |

| PayPal | $100.00 |

If your accounting system is up to date, all you’ll need to do is pull the cash balance and adjust for today’s activity. The following day, you can double check your accuracy and adjust accordingly using the last two rows.

| Daily Cash Report | |

| Book Cash Balance | $5,000.00 |

| Deposit from Today’s Sales | $900.00 |

| Merchant Deposit | $600.00 |

| Less Checks Written Today | ($1,200.00) |

| $5,300.00 | |

| Expected Bank Balance Tomorrow | $8,300.00 |

| Actual Bank Balance | $8,300.00 |

| Explain any differences |

If your accounting system is not updated in real time, you’ll need to start with the bank balance and correct it for uncleared transactions as well as list today’s activity.

| Daily Cash Report | |

| Bank Balance | $5,000.00 |

| Deposit from Today’s Sales | $900.00 |

| Merchant Deposit | $600.00 |

| Less Checks Written Today | ($1,200.00) |

| $5,300.00 | |

| Checks Still Outstanding | ($3,000.00) |

| Deposit from A/R Paid | $5,000.00 |

| Expected Bank Balance Tomorrow | $8,300.00 |

Using these formats, you can easily extend them to cover the entire week. This way, you’ll know what your cash balance will be from day to day.

If you see the value of this report for your business and would like help creating it, please reach out.

Sales tax laws are constantly changing, and sales tax audits have increased since states and local agencies have become creative about finding new ways to generate revenues. If you haven’t made any changes in your sales tax procedures in a while, you are probably at risk.

Taxability

From state to state, the taxability of items varies. For example, data processing services including web hosting and graphics are taxable in Texas but not California. Because of these intricacies, it makes sense to consult an expert in this area. Some states have been taxing certain services for many years now.

Nexus

The new buzzword in sales tax is “nexus,” which simply means presence. If your business has a presence in a state, then certain items you sell could be taxable. “Presence” is a little gray, but here are a few examples of some characteristics that the courts have decided prove nexus.

- If you have employees or contractors working in a state, you are liable to collect and remit sales tax. This can play havoc if you hire virtual or remote workers. Even if they are part-time, you have nexus in that state.

- If you outsource inventory fulfillment in any way (think Amazon sales), you have nexus in states where there is a physical warehouse that houses your products.

- If you own business property in a state, you must file sales tax.

- If you participate in trade shows or are a public speaker, you have nexus in states where the conferences are held.

The Risk

If you fail to collect taxes where you should, the risk is easy to calculate. Take the potential taxable sales times the sales tax rate, and add any penalties. The numbers get scary if you’ve been in business for several years.

Let’s say your annual revenues are $5 million. You didn’t realize that your Texas sales were taxable, and this amounts to 10% or $500K. Your tax liability is $41,250 per year. If you have been doing it wrong for five years, well, you can add it up. Add penalties on top, and it’s not a small amount. It can wipe out your entire year’s profit.

Sales tax liability becomes more important if you plan to sell your business. A traditional valuation will always include a sales tax risk analysis. Even if you don’t plan to sell, the odds of you getting audited or a disgruntled employee blowing the whistle can be too much to risk.

If you want help calculating your risk or assessing nexus or taxability for your business, reach out and we can help.

A couple of years ago, QuickBooks® gave Accounting Professionals a tool just for us – it’s only in the QuickBooks® Accountant and QuickBooks® Enterprise Accountant versions. It’s called Period Copy and it allows us to extract transactions between a set of dates for a specified period of time and condense transactions outside of the range.

This preserves transactions in the condensed file only for a particular period with entries prior to that period summarized and entries after that period removed.

This is useful for clients with file size and list limit issues as well as for third-party requests of information – not only for audit requests, but also in the event of a business sale, a divorce or legal dispute when you do not need to provide the entire QuickBooks® file.

First thing – BACKUP your data file. You are creating a new file to be issued to a third-party and you do not want to overwrite your working file.

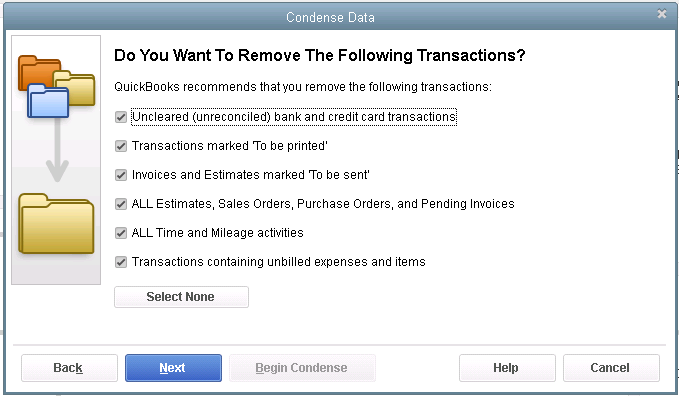

Then under the FILE menu, UTILITIES, CONDENSE DATA –

Accept the prompt that it is ok to lose Budget data.

When it prompts you for what transactions you want to remove, select “Transactions outside of a date range” to prepare a period copy of the company file. Set your before and after dates to include the period you want to keep.

Then when it prompts you how transactions should be summarized, choose “Create one summary journal entry“.

Remove the recommended transactions.

Begin Condense.

Once complete, you will have a QuickBooks® data file with only the relevant transactions for a specific period of time and you won’t be disclosing more information than need be.